The Asset‑Price State: How the U.S. Fiscal Machine Now Depends on Rising Markets

What this post argues

The U.S. does not merely like a high stock market. It increasingly needs one.

The stock market has become an amplifier inside the largest federal revenue pipe: individual income tax. When asset prices rise, capital gains, stock compensation, options, bonuses, business equity, and other asset-sensitive income strengthen federal receipts. When the market falls hard, that same amplifier runs in reverse.

This matters because the real debt problem is not debt alone. It is interest cost relative to federal revenue. If interest grows faster than normal revenue, the system becomes more dependent on asset inflation, AI valuations, national champions, and foreign capital to keep the fiscal machine stable.

That is the Asset-Price State: a system where private asset prices perform public fiscal work.

1. The three findings

This is not a new discovery in the sense that the data is hidden. The plumbing of the U.S. fiscal system is public record. The CBO publishes the revenue flows. The Federal Reserve publishes the wealth distribution. The Treasury publishes the debt. The market prices are visible every day.

What is new is the analysis of the system as a whole.

When you connect the loops, three structural realities become impossible to ignore.

-

The stock market is now a driver, not just a scoreboard. Not because every household owns stocks equally. They do not. The stock market is brutally concentrated. But structurally, the market now supports retirement wealth, collateral, corporate financing, consumer confidence, high-end spending, AI capex, national champions, and the political scoreboard of economic success. 1[6]

-

The stock market is a federal revenue engine. More than half of U.S. federal revenue comes from individual income taxes. That revenue pipe is heavily concentrated at the top, and the top of the income distribution is where stock ownership, capital gains, RSUs, options, bonuses, business equity, and taxable investment income are concentrated. 13

-

The stock market must grow to keep the debt system stable. If interest costs rise faster than ordinary revenue, the missing revenue has to come from somewhere. The politically easy sources are limited. The system can cut spending, raise taxes, default, inflate, or grow the asset base. The path it already knows how to use is asset inflation. 4

flowchart LR

A["📊 <b>1. Revenue Source</b><br/>CBO: Individual income taxes are<br/>the largest federal revenue pipe"] -->

B["🏦 <b>2. Tax Concentration</b><br/>CBO: A large share of federal taxes<br/>comes from top earners"]

B -->

C["📈 <b>3. Asset Concentration</b><br/>Fed/FRED: The top owns most stocks"]

C -->

D["🎢 <b>4. Volatility Mechanism</b><br/>CBO: Capital gains move with asset prices<br/>and are highly cyclical"]

D -->

E["⚠️ <b>5. Hidden System</b><br/>Federal revenue is amplified<br/>by stock-market performance"]

E -->

F["🔥 <b>Implication</b><br/>A prolonged market fall becomes<br/>a fiscal problem, not just a market problem"]

classDef step1 fill:#dbeafe,stroke:#1d4ed8,stroke-width:2px,color:#111827,font-weight:bold;

classDef step2 fill:#dcfce7,stroke:#15803d,stroke-width:2px,color:#111827,font-weight:bold;

classDef warn fill:#ffedd5,stroke:#ea580c,stroke-width:3px,color:#7c2d12,font-weight:bold;

classDef final fill:#fee2e2,stroke:#dc2626,stroke-width:3px,color:#7f1d1d,font-weight:bold;

class A,B step1;

class C,D step2;

class E warn;

class F final;

linkStyle 0 stroke:#1d4ed8,stroke-width:2px;

linkStyle 1 stroke:#15803d,stroke-width:2px;

linkStyle 2 stroke:#15803d,stroke-width:2px;

linkStyle 3 stroke:#ea580c,stroke-width:3px;

linkStyle 4 stroke:#dc2626,stroke-width:3px;

1.1 The revenue pipe

The Treasury’s own revenue data makes the first part of the argument impossible to ignore.

The largest source of U.S. federal revenue is not corporate tax. It is not tariffs. It is not customs duties. It is not some obscure financial levy.

It is individual income tax.

So far in FY2026, individual income taxes account for roughly 52% of total federal revenue. Social Security and Medicare taxes account for another 34%. Everything else is smaller.

That means the U.S. fiscal machine depends first and foremost on taxing individual income.

But “individual income” is not just wages.

At the top of the distribution, individual income includes capital gains, stock options, RSUs, bonuses, business equity, taxable investment income, and other asset-linked flows.

This is where the stock market enters the system.

The stock market does not literally appear as a single line item called “stock market revenue” in the Treasury tables. That would be too simple.

Instead, it hides inside the largest pipe.

When asset prices rise, high-income taxable income rises disproportionately. Capital gains are realised. Stock compensation becomes more valuable. Options are exercised. RSUs vest. Bonuses expand. Business valuations rise. High-end consumption holds up.

Some of that private asset inflation becomes public revenue.

That is the Asset-Tax Amplifier.

The stock market is not the largest federal revenue category directly.

It is more important than that.

It is the amplifier inside the largest federal revenue category.

1.2 The spending curve does not flatten

Before we model the stock market, we need to model the spending side.

Because one of the quiet assumptions in normal political debate is that the government can somehow hold spending steady.

That assumption is fantasy.

The U.S. federal budget is not a normal household budget. It is a machine with built-in escalators: Social Security, Medicare, health care costs, defence commitments, debt interest, industrial policy, crisis response, and the political cost of cutting anything people have already come to expect.

The spending curve does not flatten by itself.

CBO’s baseline already shows the problem. Federal outlays are projected to rise from roughly $7.4 trillion in 2026 to $11.4 trillion by 2036. Revenues also rise, but not enough. The deficit still grows from roughly $1.9 trillion to $3.1 trillion over the same period. [S1]

That is under baseline assumptions.

Not crisis assumptions.

Not recession assumptions.

Not war assumptions.

Not banking-system-rescue assumptions.

Just baseline.

This is why the idea that the U.S. can simply “grow out of it” without changing the revenue engine is weak. Spending is already programmed upward. Interest costs are already rising. Mandatory spending is already politically difficult to cut. The system does not need one bad year to become unstable. It only needs the existing curves to keep doing what they are already doing.

That is the fiscal background to the stock-market argument.

The stock market is not just currently important to federal revenue. It needs to become more important.

This is the key point.

If spending keeps rising, and interest keeps rising, and ordinary revenue growth is not enough, then the missing revenue has to come from somewhere.

Payroll taxes cannot double without crushing labour.

Corporate taxes are too small a pipe.

Tariffs are unstable and inflationary.

Spending cuts are politically brutal.

Explicit tax hikes are politically dangerous.

That leaves the easiest politically scalable mechanism the system already knows how to use:

asset inflation.

Push asset prices higher. Let the top of the income distribution realise gains. Let RSUs vest at higher values. Let options become valuable. Let bonuses expand. Let business valuations rise. Let high-end consumption continue. Let capital gains and asset-linked income flow into the individual income-tax system.

The stock market does not simply need to stay high.

It needs to grow into the gap.

That is why the next stage of the model is not just:

“How high are stocks?”

It is:

“How high do stocks need to go for the revenue system to keep pace with the spending and interest curve?”

graph LR

A["💸 Spending is not flat"] --> B["📈 Interest is the fastest-growing pressure"]

B --> C["💵 Revenue is concentrated in individual income taxes"]

C --> D["👑 Income taxes are concentrated at the top"]

D --> E["💹 The top is asset-price-sensitive"]

E --> F["🏛️ Therefore the stock market must carry more of the system over time"]

style A fill:#f9d,stroke:#333,stroke-width:2px,color:#000

style B fill:#bbf,stroke:#333,stroke-width:2px,color:#000

style C fill:#bfb,stroke:#333,stroke-width:2px,color:#000

style D fill:#ffd,stroke:#333,stroke-width:2px,color:#000

style E fill:#fdd,stroke:#333,stroke-width:2px,color:#000

style F fill:#ddf,stroke:#333,stroke-width:2px,color:#000

1.3 Interest versus revenue: the rollover problem

The next part of the model is interest.

This is where the system becomes dangerous.

At first glance, the U.S. debt burden looks manageable because the current average interest rate on the debt is still relatively low. The blended cost is around the low-three-percent range.

But that number is backward-looking.

It reflects the average cost of debt issued across many previous years, including years when rates were close to zero. It is not the true cost of issuing or rolling debt in the current market.

That distinction matters.

The U.S. is not refinancing a small loan. It is constantly rolling an enormous stock of debt. As old debt matures, it has to be refinanced at current market rates. If current rates are higher than the blended rate, the interest burden rises even if nothing else changes.

This is the rollover problem.

The U.S. is still paying yesterday’s blended debt cost, but it must refinance into today’s rate environment.

That is why this section models interest rates from 4% to 12%.

Not because 12% is the base case.

It is not.

But because the system needs to be stress-tested.

A debt system that looks survivable at 3.3% can become structurally different at 5%. At 7.5%, it starts consuming the budget. At 10% or 12%, it becomes a political and monetary emergency.

The important question is not simply:

“How much debt does the U.S. have?”

The better question is:

“At what interest rate does the debt stock begin to overwhelm the revenue system?”

That is what we model next.

1.4 The rollover stress model

We model the debt burden in two ways.

First, we model the debt stock growing normally over time.

Debt(t) = Debt(0) × (1 + debt_growth_rate)^t

This gives us the normal debt curve.

Then we apply different effective interest rates to that debt stock.

Interest(t) = Debt(t) × effective_interest_rate

The interest-rate scenarios are:

4%

5%

7.5%

10%

12%

This is not a precise Treasury maturity model. A full model would use the maturity schedule, bill/note/bond composition, auction calendar, inflation assumptions, and CBO rate path.

But that is not the purpose here.

The purpose is to expose the scale of the pressure.

If the debt stock is roughly stable, a higher interest rate increases the interest bill directly. If the debt stock keeps growing, the interest burden compounds.

That gives us the first curve:

normal debt growth

→ effective rollover rate

→ annual interest burden

The second curve is revenue.

Revenue(t) = Revenue(0) × (1 + normal_revenue_growth_rate)^t

Now we can compare the two.

If revenue grows at 4% but interest grows at 7%, 10%, or 12%, the gap widens quickly.

That gap is the problem.

The government has to close it somehow.

2. The inflation signal

The official Federal Reserve target is still 2%.

But the more important question is no longer simply:

Is inflation above target?

Yes.

Headline CPI peaked at 8.58% in 2022 Q2, then fell through 2023–2025, but re-accelerated to 3.87% in 2026 Q2. Core CPI peaked at 6.33% in 2022 Q1 and still sits at 2.68% in 2026 Q2 — above the Fed’s 2% target.

The important point is not just that inflation surged in 2021–2022.

It is that inflation has not cleanly returned to target after years of tightening.

So the better question is:

What does the Fed do when inflation remains above target, but raising rates aggressively would damage the debt system, the stock market, the housing market, and the federal revenue machine?

That is the corridor we are entering.

If the Fed raises rates hard enough to crush inflation, it also raises the effective cost of refinancing U.S. debt. The government is still paying a blended debt cost inherited from earlier, lower-rate years. But as debt rolls over, today’s rates become tomorrow’s interest bill.

That is the trap.

The Fed cannot ignore inflation.

But it also cannot treat inflation as the only variable in the system.

Inflation is now entangled with:

debt service

Treasury refinancing

stock-market valuations

housing affordability

bank balance sheets

AI capex

federal tax receipts

dollar credibility

This is why the measurement layer matters.

If policymakers begin emphasizing alternative inflation measures, temporary effects, trimmed-mean inflation, or broader “underlying” gauges, that does not automatically mean the 2% target has been abandoned.

But it does show how constrained systems behave.

When a system cannot solve a problem directly, it starts changing which signal it treats as decisive.

That is not conspiracy.

It is systems behaviour.

A central bank facing above-target inflation, rising debt-service pressure, fragile asset prices, and political demand for lower rates has an incentive to distinguish between two kinds of inflation.

Bad inflation de-anchors expectations and forces rate hikes.

Tolerable inflation lifts nominal GDP, raises nominal tax receipts, supports asset prices, and reduces the real burden of old debt.

That distinction is where the fiscal system enters monetary policy.

The stock market needs liquidity.

The Treasury needs manageable rates.

The government needs revenue.

The debt stock benefits from inflation.

The public needs prices to stop rising.

Those goals cannot all be maximized at the same time.

So policy becomes an exercise in choosing which pain can be delayed, renamed, or distributed.

That is why inflation belongs near the top of this post.

The Asset-Price State does not work without it.

The system needs inflation high enough to lift nominal revenue and asset prices, but not so high that the bond market revolts or the public loses faith in the currency.

That is the narrow path:

high enough inflation to dilute the debt

low enough inflation to preserve credibility

low enough rates to protect debt service

high enough stocks to support federal revenue

This is the policy corridor.

The Fed may still talk about 2%.

But the system increasingly behaves as if the real target is not simply low inflation.

The real target is controlled inflation plus high asset prices.

That is what keeps the machine alive.

3. Why this is an AI post, not a finance rant

programmer.ie is about AI, systems, software, and modelling.

So this post is not about predicting next month’s S&P 500 move.

It is not a claim that some hidden room in Washington sets stock prices.

It is an attempt to model a complex system whose effects are visible, but whose internal mechanism is easy to miss until the flows are connected.

The stock market rises.

Mega-cap valuations stretch.

AI infrastructure spending explodes.

SpaceX becomes a multi-trillion-dollar object.

Policymakers panic when markets fall.

The dollar remains dominant even as purchasing power weakens.

Foreign companies become cheap relative to U.S. companies.

Those are symptoms.

The system is underneath.

That is where AI becomes useful.

Not because AI can predict the future.

It cannot.

Not because AI knows where the market will trade next quarter.

It does not.

The value of AI here is different.

AI is useful for decomposing a messy system into variables, assumptions, feedback loops, and failure thresholds.

That is what we used it for.

The starting intuition was simple:

The U.S. seems increasingly dependent on a rising stock market.

That is not a model.

It is a suspicion.

AI helped turn that suspicion into a stress-testable chain:

graph LR

A["📈 Debt growth"] --> B["💸 Interest burden"]

B --> C["🏛️ Federal revenue"]

C --> D["📊 Asset-sensitive tax receipts"]

D --> E["🚀 Required stock-market growth"]

E --> F["🌐 Global consequences"]

style A fill:#ffcccc,stroke:#b30000,stroke-width:2px,color:#000

style B fill:#ffe0cc,stroke:#cc5500,stroke-width:2px,color:#000

style C fill:#ffffcc,stroke:#b3b300,stroke-width:2px,color:#000

style D fill:#ccffcc,stroke:#2d862d,stroke-width:2px,color:#000

style E fill:#cce5ff,stroke:#004080,stroke-width:2px,color:#000

style F fill:#e6ccff,stroke:#5900b3,stroke-width:2px,color:#000

Each part of that chain is public.

The debt is public.

The interest cost is public.

The revenue mix is public.

The concentration of stock ownership is public.

The concentration of income-tax payments is public.

The volatility of capital-gains receipts is public.

The missing step is the system connection.

That is the AI part of the post.

The formulas are simple on purpose.

The goal is not to hide the argument inside a black box.

The goal is to make the argument inspectable.

AI was used as a systems-modelling partner:

intuition

→ decomposition

→ variable selection

→ assumption extraction

→ scenario design

→ adversarial critique

→ simple model

→ human audit

The useful questions were not:

What will the stock market do?

The useful questions were:

Where does stock-market wealth enter federal revenue?

What happens if interest costs rise faster than normal revenue?

Which revenue channels are asset-sensitive?

What assumptions would make the model fail?

What happens if the market falls instead of rises?

At what point does required market growth exceed believable earnings growth?

That is a different use of AI.

Not oracle.

Not ghostwriter.

Not market predictor.

Stress harness.

A programmer would recognise the pattern immediately.

You have a system with inputs, outputs, hidden dependencies, feedback loops, and failure thresholds. You do not understand it by staring at one log line. You build a model. You vary the inputs. You watch where the system leaves normal operating range.

That is what this post does.

It takes the U.S. fiscal machine and stress-tests it under different interest-rate environments:

4%

5%

7.5%

10%

12%

Then it compares those interest paths against normal revenue growth.

Then it asks how much extra revenue would be needed to keep the interest burden from overwhelming the system.

Then it asks how much of that revenue could plausibly come from the Asset-Tax Amplifier.

That produces the important curve:

required stock-market growth

Without the model, “the government needs the stock market high” sounds like a political slogan.

With the model, it becomes a structural question:

At what point does the required stock-market growth become larger than believable earnings growth?

That is where the system becomes unstable.

Not when the stock market is high.

Not when valuations look expensive.

Not even when interest costs rise.

The danger point is when the market has to grow faster than the real economy can justify simply to keep the fiscal machine functioning.

That is the moment the market stops behaving like a normal market and starts behaving like a survival mechanism.

This is why the post connects AI, SpaceX, mega-cap technology, inflation, interest rates, federal revenue, and dollar dominance.

They are not separate stories.

They are one system.

And the purpose of AI here is to make that system visible enough to test, challenge, and attack.

The question is simple:

When does it become impossible?

4. Systems thinking: reality is made of loops

People misread economies because they look at events instead of patterns.

An event is easy to see.

The Fed cuts rates.

Stocks rally.

Inflation rises.

Treasury yields move.

SpaceX IPOs.

Gold rises.

Europe weakens.

Each of these looks like a separate story. Each one gets its own headline, its own analyst note, its own explanation.

But the economy is not a list of events.

It is a machine of loops.

A system looks more like this:

graph LR

A["📈 Stocks support wealth"] --> B["💰 Wealth supports tax revenue"]

B --> C["🧾 Tax revenue supports debt service"]

C --> D["💳 Debt service pressures policy"]

D --> E["⚖️ Policy supports stocks"]

E --> A

style A fill:#ffe0cc,stroke:#ff8c00,stroke-width:2px,color:#000

style B fill:#e0f7fa,stroke:#00acc1,stroke-width:2px,color:#000

style C fill:#e8f5e9,stroke:#43a047,stroke-width:2px,color:#000

style D fill:#fff3e0,stroke:#fb8c00,stroke-width:2px,color:#000

style E fill:#f3e5f5,stroke:#8e24aa,stroke-width:2px,color:#000

Once you see the loop, the behaviour becomes less surprising.

Governments do not need to sit in a room and consciously design every outcome. They respond to pressure. They protect the parts of the system that have become load-bearing. They choose the option that causes the least immediate breakage. Over time, those choices become a pattern.

That pattern is the system.

This is why market intervention keeps returning under different names. One decade it is quantitative easing. Another decade it is emergency liquidity. Another decade it is bank support, fiscal transfers, special facilities, industrial policy, or national-security investment.

The label changes.

The loop does not.

The state protects the market because the market now protects parts of the state.

That is the point of this post.

If you treat the stock market as an event-driven casino, the behaviour looks absurd. Valuations look insane. Policy looks inconsistent. Politicians look obsessed with a scoreboard that only reflects the wealth of a minority.

But if you treat the stock market as part of the fiscal architecture, the behaviour becomes easier to understand.

The market supports wealth.

Wealth supports tax receipts.

Tax receipts support debt service.

Debt service pressures policy.

Policy supports the market.

The system closes around itself.

Winter is not an event. It is a pattern. If you misunderstand the pattern, reality punishes you.

The same is true here.

The U.S. stock market is no longer just reacting to the economy.

It has become one of the loops through which the American state maintains itself.

5. The previous posts: from interest/revenue to asset inflation

This post is the fourth part of a sequence.

In the first post, I argued that the most useful way to understand U.S. fiscal pressure is not total debt, and not even total interest expense in isolation.

The key metric is:

Interest as a percentage of federal revenue.

Revenue is oxygen.

Interest is the cost of yesterday.

A state can carry a large debt burden if the cost of that debt remains manageable relative to the revenue system that supports it. But once interest grows faster than revenue, fiscal flexibility collapses. At that point the problem is no longer abstract. It becomes a constraint on what the state can do.

That first post used AI to turn a vague question — “Is U.S. debt becoming a problem?” — into a measurable systems question:

When does interest on U.S. debt become a constraint on the system?

The answer was not collapse.

It was constraint.

An increasing share of government resources becomes consumed by past obligations. That reduces flexibility, increases trade-offs, and makes the system more sensitive to shocks.

The second post then asked a different question.

If the debt curve is becoming harder to sustain, how does the system extend the cycle?

One answer is currency devaluation.

Not necessarily a dramatic overnight collapse. Not necessarily a declared policy. More likely a gradual adjustment through inflation, nominal repricing, asset inflation, and real purchasing-power erosion.

That post framed devaluation as a silent reset.

The debt does not disappear.

The burden is shifted.

Nominal GDP rises. Nominal tax receipts rise. The real value of old debt falls. Asset prices adjust upward. Savers and wage earners absorb part of the loss through reduced purchasing power.

But this post adds the missing mechanism.

The U.S. does not need to devalue only through the visible exchange rate.

It can devalue through the asset base.

This is a more advanced form of currency arbitrage.

Instead of simply weakening the dollar in a way everyone can see, the system can inflate U.S. asset prices.

That does several things at once.

It increases the taxable income of the asset-owning class.

It strengthens federal revenue through the individual income-tax system.

It makes U.S. companies vastly richer in market-cap terms.

It gives those companies acquisition power over foreign competitors.

It allows American firms to buy real global assets using inflated equity.

It forces foreign investors to chase U.S. markets or fall behind.

It exports inflationary pressure through the dollar system without requiring a single formal devaluation event.

This is the deeper mechanism.

The reset is not only:

weaken the dollar

→ reduce real debt

→ inflate nominal revenue

It is also:

inflate U.S. asset prices

→ expand asset-linked taxable income

→ strengthen federal revenue

→ increase U.S. corporate purchasing power

→ export valuation pressure globally

→ make foreign assets cheap relative to U.S. equity

That is why the stock market matters.

It is not simply a scoreboard.

It is not simply a bubble.

It is not merely a rich-person wealth effect.

It is becoming part of the fiscal machinery of the state.

The earlier posts showed the pressure:

interest grows faster than revenue

Then they showed the traditional escape valve:

currency devaluation and inflation

This post shows the operational mechanism:

asset inflation as fiscal support

That is the new layer.

The U.S. can preserve the appearance of dollar strength while inflating the dollar value of its own asset base. It can maintain global demand for dollars while allowing the purchasing power of those dollars to decay. It can keep foreign capital inside the U.S. market by making the U.S. market the only game large enough to absorb global savings.

This is why the phrase “currency devaluation” is no longer enough.

The more accurate phrase is:

asset-price devaluation of the currency.

The dollar may not collapse on a foreign-exchange chart.

But if the price of everything important — stocks, houses, AI companies, strategic infrastructure, defence contractors, energy assets — rises faster than wages and foreign market values, then the currency has still been devalued.

It has just been devalued through assets instead of through a single exchange-rate event.

That is what this post models.

We are not asking whether the stock market is high.

We are asking a harder question:

How high does the stock market need to go for the U.S. revenue system to keep pace with the debt and interest curve?

flowchart LR

A["🧮 Post 1<br/><b>Interest / Revenue</b><br/>Debt becomes a constraint when interest grows faster than revenue"] -->

B["📉 Post 2<br/><b>Silent Reset</b><br/>Inflation and currency adjustment extend the debt cycle"]

B -->

C["📈 This Post<br/><b>Asset-Price State</b><br/>Stock-market inflation becomes the operational revenue mechanism"]

C -->

D["🏛️ Fiscal Effect<br/>Asset-linked income rises<br/>Federal tax receipts strengthen"]

C -->

E["🌍 Global Effect<br/>U.S. companies gain purchasing power<br/>Foreign assets become cheaper in relative terms"]

C -->

F["💵 Currency Effect<br/>The dollar can look stable<br/>while purchasing power erodes through asset inflation"]

classDef prior fill:#dbeafe,stroke:#1d4ed8,stroke-width:2px,color:#111827;

classDef current fill:#ffedd5,stroke:#ea580c,stroke-width:3px,color:#7c2d12;

classDef effect fill:#dcfce7,stroke:#15803d,stroke-width:2px,color:#111827;

class A,B prior;

class C current;

class D,E,F effect;

the fourth post will be explained later

6. The problem statement: the machine has too many plates

The problem is not simply that the United States has too much debt.

That is too vague.

The problem is that the U.S. fiscal machine now has to keep several unstable variables balanced at the same time.

It needs spending to continue, because the spending curve does not flatten.

It needs interest rates low enough that the debt stock can be rolled over without the interest bill exploding.

It needs inflation high enough to raise nominal GDP, nominal tax receipts, and asset prices.

It needs inflation low enough that the bond market does not revolt.

It needs the stock market high enough to support household wealth, confidence, capital gains, RSUs, options, bonuses, business valuations, pension assets, and federal income-tax receipts.

It needs AI and strategic companies to justify valuations that would look insane under normal earnings logic.

It needs foreign capital to keep buying U.S. assets.

It needs the dollar to remain trusted, even while the purchasing power of the dollar is being quietly diluted.

That is the balancing act.

The state is not trying to solve one problem.

It is trying to keep several plates spinning.

debt cannot grow too fast

interest cannot rise too far

inflation cannot fall too low

inflation cannot rise too high

stocks cannot fall too far

Treasury demand cannot break

AI valuations cannot lose credibility

the dollar cannot lose reserve status

This is why normal political language is misleading.

People talk as if the government has a clean menu of options:

cut spending

raise taxes

default

inflate

grow productivity

increase asset-linked revenue

But most of those options are either politically impossible, too slow, or systemically dangerous.

Cutting spending is politically brutal.

Raising taxes is politically dangerous.

Default is unthinkable.

Productivity growth takes time.

Inflation helps the debt, but damages trust.

Higher interest rates fight inflation, but worsen the debt-service problem.

Lower interest rates help debt service and asset prices, but risk reigniting inflation.

So the system reaches for the path that does the most things at once:

Keep rates lower than inflation would normally justify, keep the stock market high, let asset prices rise, and allow taxable income at the top to expand federal revenue without openly calling it a tax increase.

That is the hidden elegance of the mechanism.

It is not one policy.

It is a coordination problem.

The Treasury, the Fed, the White House, the stock market, the AI complex, and the largest companies all become part of the same machine.

The Treasury has to finance the deficit.

The Fed has to prevent inflation from breaking credibility while also preventing rates from breaking the fiscal system.

The White House needs the stock market as a political scoreboard.

The stock market needs a growth story large enough to absorb global capital.

The AI companies provide that story.

The mega-cap companies provide the index weight.

Foreign investors provide the demand.

And the tax system converts part of the resulting asset inflation into federal revenue.

That is the actual problem.

Not “how does the U.S. pay its debt?”

The deeper question is:

How does the U.S. keep the asset machine large enough to support the debt machine?

This is where the market concentration matters.

If the S&P 500 were rising because all 500 companies were growing together, that would suggest broad economic strength.

But if the index is being pulled upward by a small number of mega-cap companies, then something different is happening.

The market is not simply measuring the economy.

It is concentrating the economy into a handful of firms large enough to carry the index, attract global capital, justify AI infrastructure spending, and expand the asset base.

That is why we need to split the market in the model.

We should not only look at the S&P 500.

We should compare:

S&P 500 market-cap weighted

S&P 500 equal-weight

Magnificent Seven / top AI infrastructure complex

S&P 493

If the market-cap-weighted index rises while the equal-weight index stagnates, that tells us the growth is not broad.

It tells us the system is becoming more dependent on a narrow layer of companies.

That matters because the Asset-Tax Amplifier does not require every company to rise equally.

It only requires enough market-cap expansion at the top to create taxable income, capital gains, stock compensation, and confidence.

This is why the next phase of the model cannot simply ask:

How much must the stock market grow?

It has to ask:

Where must the stock market grow?

Because the fiscal machine does not need every stock to become more valuable.

It needs the taxable asset base to expand.

And in the modern U.S. market, that increasingly means the largest companies, the AI companies, the national champions, and the firms capable of carrying trillion-dollar valuations.

This is where the problem becomes uncomfortable.

The U.S. does not merely need a strong economy.

It needs a strong enough stock market.

It does not merely need a strong enough stock market.

It needs enough growth in the part of the stock market owned by the people who pay the most taxes.

And it does not merely need that growth to happen once.

It needs it to keep happening as spending rises, debt rolls over, and interest costs climb.

That is the machine.

The next section models how large the machine has to become.

6.1 The players/plates table

| Player | Plate they are juggling | What they need | Failure mode |

|---|---|---|---|

| Treasury | Deficit financing and debt rollover | Strong demand for Treasuries, manageable yields | Interest bill explodes |

| Fed | Inflation, rates, liquidity | Inflation tolerated but not uncontrolled; rates low enough not to break debt | Either inflation credibility breaks or asset/debt system breaks |

| White House | Political legitimacy | High stock market, strong nominal growth, visible prosperity | Market fall becomes political crisis |

| Stock market | Wealth, collateral, tax base | Rising valuations and liquidity | Capital gains/tax receipts weaken |

| Mega-cap companies | Index support | Earnings story, buybacks, AI capex credibility | Index loses narrow support |

| AI complex | Growth narrative | A believable productivity/infrastructure boom | Valuation story breaks |

| Foreign investors | Dollar recycling | U.S. assets remain the dominant place to park capital | Dollar/Treasury demand weakens |

| Tax system | Revenue conversion | Asset gains become taxable income | Revenue gap widens |

flowchart LR

A["🏛️ Treasury<br/>Finance deficits<br/>Roll debt"] --> H["⚖️ The Balancing Problem"]

B["🏦 Fed<br/>Rates + inflation<br/>Liquidity backstop"] --> H

C["🧢 White House<br/>Political scoreboard<br/>Market confidence"] --> H

D["📈 Stock Market<br/>Wealth + collateral<br/>Taxable gains"] --> H

E["🤖 AI Complex<br/>Growth story<br/>Capex justification"] --> H

F["🏢 Mega-Caps<br/>Index weight<br/>Trillion-dollar containers"] --> H

G["🌍 Foreign Capital<br/>Dollar recycling<br/>Asset demand"] --> H

H --> I["🔥 Required Outcome<br/>Low-enough rates<br/>High-enough inflation<br/>High-enough stocks<br/>Believable-enough growth"]

I --> J["💰 Asset-Tax Amplifier<br/>Stock gains become<br/>taxable federal revenue"]

classDef actor fill:#dbeafe,stroke:#1d4ed8,stroke-width:2px,color:#111827;

classDef balance fill:#ffedd5,stroke:#ea580c,stroke-width:3px,color:#7c2d12;

classDef outcome fill:#dcfce7,stroke:#15803d,stroke-width:2px,color:#111827;

classDef final fill:#fee2e2,stroke:#dc2626,stroke-width:3px,color:#7f1d1d;

class A,B,C,D,E,F,G actor;

class H balance;

class I outcome;

class J final;

7. Why Trump points at the stock market

Trump points at the stock market because he understands the dashboard.

This is not really about Trump.

He is simply more explicit than other presidents.

Every modern U.S. administration is constrained by the same pressure system. The difference is that Trump says the quiet part out loud. He treats the stock market as proof that the country is winning because, politically, that is increasingly how the American system behaves.

The stock market is not the whole economy.

But it has become the visible control panel.

It signals:

retirement confidence

consumer confidence

business confidence

capital gains

tax receipts

corporate financing

AI leadership

national prestige

dollar credibility

That is why market pressure changes political behaviour.

When a president announces an aggressive policy, markets immediately translate it into system pressure.

The pressure dashboard has four main dials:

| Dial | What it measures | Why it matters |

|---|---|---|

| S&P 500 | Asset prices and confidence | Falling stocks damage wealth, pensions, capital gains, and political legitimacy |

| 10-year Treasury yield | Cost of money | Rising yields increase borrowing costs and signal bond-market stress |

| Inflation | Cost-of-living pressure | High inflation hurts voters directly and limits the Fed’s ability to cut |

| Approval rating | Political tolerance | Weak polling reduces the president’s room to absorb economic pain |

This is the real point.

A president does not need to be secretly controlled by Wall Street for markets to discipline him.

The discipline is built into the system.

If stocks fall, yields rise, inflation stays high, and approval weakens, the political cost of extreme policy rises quickly. The president can still continue. But the system begins to push back.

That pushback is visible in the pattern:

aggressive policy threat

→ markets sell off

→ yields rise or liquidity tightens

→ inflation risk increases

→ approval pressure builds

→ policy softens, delays, or gets renamed

→ markets recover

That is not weakness in the personal sense.

It is system pressure.

The stock market matters here because it is the fastest-moving political signal. Polls lag. Economic data lags. Tax receipts lag. But the market reprices instantly.

This makes the S&P 500 a real-time referendum on policy.

That does not mean the market is always right.

It means the market is fast.

And in a system where asset prices support tax revenue, household wealth, corporate financing, and political legitimacy, a fast signal becomes a powerful signal.

This is why Trump keeps returning to the market.

He treats it as the score because the system has made it the score.

But the deeper point is that the score itself has changed.

In an older economy, a president could point to wages, factories, employment, trade balances, or production.

In the current system, the headline market index has become the compressed signal for everything the state needs to preserve:

wealth

confidence

liquidity

tax receipts

capital formation

AI investment

dollar demand

That is why this post keeps coming back to the stock market.

Not because the stock market represents ordinary life.

It does not.

But because it represents the part of the system that the state cannot easily allow to break.

Once the market falls far enough, it stops being a market event.

It becomes a political event.

Then a fiscal event.

Then a policy event.

That is the feedback loop.

Trump sees the dashboard.

The market sees that he sees it.

And once markets believe a president has a pain threshold, they begin trading against that threshold.

That is how a market becomes a policy constraint.

8. The Asset-Tax Amplifier

This is the heart of the analysis.

Everything before this section points here.

The debt is the stock.

Interest is the pressure.

Revenue is the oxygen.

And the stock market is the amplifier inside the largest revenue pipe.

That is the system.

The United States can carry a large debt burden as long as the revenue system can support the interest cost. The debt itself is not the immediate problem. The problem is what happens when the interest bill grows faster than the state’s ability to collect revenue.

That is why federal revenue matters so much.

And the largest source of federal revenue is individual income tax.

Not corporate tax.

Not tariffs.

Not customs duties.

Individual income tax.

That means the fiscal survival of the U.S. state depends heavily on the income-tax pipe.

But that pipe is not evenly distributed.

It is concentrated at the top.

And the top of the income distribution is where the stock market lives.

Capital gains.

RSUs.

Stock options.

Bonuses.

Executive compensation.

Business equity.

Taxable investment income.

High-end consumption.

That is the bridge.

The stock market does not appear in the federal accounts as a line item called “stock-market revenue.” It is more hidden than that. It flows through individual income tax.

When the stock market rises, the asset-owning class gets richer. Some of that wealth remains unrealised, but enough becomes taxable to matter.

Capital gains are realised.

Options are exercised.

RSUs vest.

Bonuses expand.

Business valuations rise.

Founders sell shares.

Executives pay tax on compensation.

High-end spending continues.

Some of that private asset inflation becomes public revenue.

That is the Asset-Tax Amplifier.

stock market rises

→ asset-owning households become richer

→ capital gains, RSUs, options, bonuses, and business income rise

→ top-decile taxable income rises

→ individual income-tax receipts strengthen

→ federal revenue improves

→ debt-service pressure becomes easier to manage

And the reverse is just as important:

stock market falls hard

→ capital gains collapse

→ stock compensation loses value

→ bonuses compress

→ business valuations fall

→ taxable high-end income weakens

→ individual income-tax receipts weaken

→ deficit pressure worsens

→ policy is pulled toward intervention

This is why a prolonged market crash is no longer just a market event.

It becomes a revenue event.

Then a deficit event.

Then a debt-service event.

Then a policy event.

That is the loop.

The stock market is not merely enriching the wealthy.

It is feeding the state.

The important point is not that all federal revenue comes from stocks. It does not.

The point is more precise:

The largest federal revenue pipe is individual income tax, and the volatile upside of that pipe is highly exposed to asset prices.

That is what changes the whole system.

If interest costs are stable, the Asset-Tax Amplifier is helpful but not existential.

But if interest costs double over the next five to ten years, the amplifier becomes structurally important.

The state cannot easily double payroll taxes.

It cannot easily double corporate taxes.

It cannot easily double tariffs without breaking trade and raising inflation.

It cannot easily cut spending enough to offset the interest curve.

So the system looks for the one revenue channel that can expand without being announced as a tax increase.

Asset prices.

Push the market higher.

Let taxable gains appear.

Let compensation rise.

Let the top decile carry more of the revenue load.

Let the stock market grow into the gap.

That is the mechanism this post is modelling.

The next section does not ask whether the stock market is high.

It asks something more uncomfortable:

How high does the stock market need to go to keep the U.S. fiscal machine ahead of the interest curve?

Because if interest doubles, revenue has to grow somewhere.

And if ordinary revenue cannot grow fast enough, the system must either accept constraint, impose pain, or inflate the asset base.

That is why the stock market matters.

It is no longer just a scoreboard.

It is no longer just a casino.

It is no longer just Wall Street wealth.

It is a fiscal support structure.

And once a market becomes part of the revenue system, policymakers stop treating it like a normal market.

9. The model: what we asked the AI to calculate

This is where the post stops being an argument and becomes a model.

Everything up to this point has been setup.

We know the problem.

The U.S. has rising debt.

It has rising interest costs.

It has spending that does not flatten.

It has inflation above target.

It has a federal revenue system heavily dependent on individual income taxes.

And the volatile upside of that tax pipe is exposed to asset prices.

So the question becomes quantifiable.

If interest costs rise faster than normal federal revenue, how much must the stock market grow to keep the U.S. fiscal machine stable?

That is what we asked the model to calculate.

We used AI not to predict the market, but to build a stress harness.

The model has one purpose:

Show when the system leaves normal ranges.

The inputs are simple:

starting federal revenue

starting federal debt

current net interest cost

normal revenue growth rate

normal debt growth rate

effective rollover interest rate

asset-sensitive tax base

target interest/revenue ratio

The interest-rate scenarios are:

4%

5%

7.5%

10%

12%

The time horizons are:

1 year

5 years

10 years

The inflation assumption is also important.

We assume inflation remains around 4%.

That means the model gives the government credit for nominal revenue growth. It does not assume deflation. It does not assume collapse. It assumes inflation helps lift nominal tax receipts.

Even with that help, the system becomes strained quickly.

The core question is:

How much must the stock market grow to produce enough asset-sensitive tax revenue to stop interest from consuming a larger share of federal revenue?

That is the Required Market Curve.

It is the curve this post has been building toward.

10. The maths

The model uses a deliberately simple structure.

First, debt grows over time:

Debt(t) = Debt(0) × (1 + debt_growth_rate)^t

Then we apply an effective interest rate:

Interest(t) = Debt(t) × effective_interest_rate

Revenue grows with inflation and nominal activity:

Revenue(t) = Revenue(0) × (1 + normal_revenue_growth_rate)^t

We then preserve the current interest burden as the target ratio:

TargetInterest(t) = Revenue(t) × current_interest_to_revenue_ratio

The model then calculates the gap:

RevenueGap(t) = Interest(t) - TargetInterest(t)

Finally, we ask how much the asset-sensitive tax base would need to expand to close that gap:

RequiredMarketMultiple =

1 + RevenueGap(t) / AssetSensitiveTaxBase

This is not a precise Treasury maturity model.

A full model would include:

bill / note / bond maturity schedule

weighted-average maturity

coupon structure

new issuance

inflation-indexed debt

foreign demand

Federal Reserve balance-sheet policy

tax-realisation behaviour

market drawdowns

That is not the goal here.

The purpose of this model is not exact accounting.

The purpose is to expose scale.

A model does not need to be perfect to be useful.

It only needs to show when the system leaves normal operating range.

And under higher effective interest rates, it does.

At 4%, the system is already approaching constraint.

At 5%, the interest burden becomes meaningfully uncomfortable.

At 7.5%, the burden becomes severe.

At 10% or 12%, the model stops looking like normal public finance and starts looking like emergency fiscal arithmetic.

That is the point.

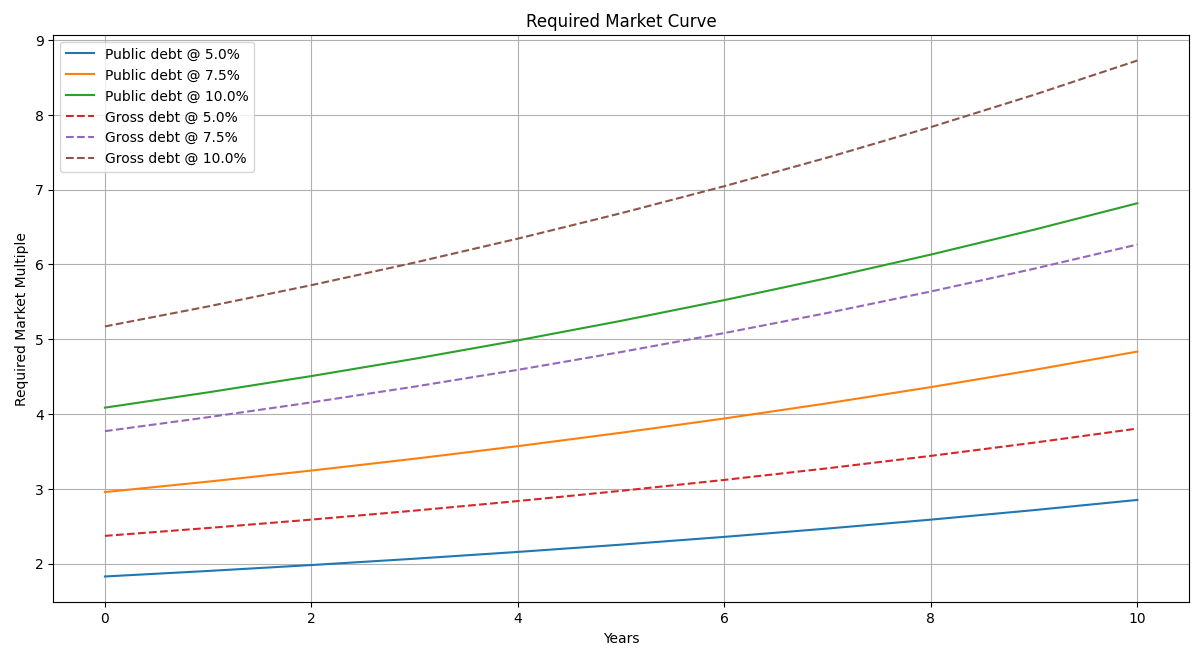

11. The result: the Required Market Curve

The AI generated the Required Market Curve.

This is the point where the argument stops being conceptual and becomes visual.

The curve answers a specific question:

How much does the stock-market-linked tax base need to expand to stop interest from consuming a larger share of federal revenue?

To make the result as clear as possible, I show the model two ways.

First, using debt held by the public — the cleaner measure of market-facing debt, and the fairest base for a refinancing and interest-rate stress model.

Second, using gross federal debt — the larger headline number that includes intragovernmental holdings, and the number most readers think of when they hear that U.S. debt is approaching $40 trillion.

This matters because both numbers are real, but they describe different layers of the system.

The result is stark.

At a 5% effective interest rate, the required market expansion is already large. The asset-sensitive tax base has to grow aggressively just to keep the interest-to-revenue ratio flat.

At 7.5%, the system becomes extreme. The market has to do far more than reflect economic growth. It has to carry fiscal pressure.

At 10%, the model starts producing numbers that are difficult to reconcile with traditional valuation logic. The required expansion pushes toward permanent, aggressive multiple growth.

And when the model is run against the full gross-debt headline, the required expansion becomes even more severe.

That is the point of the curve.

It is not predicting that the market will literally rise by one exact multiple.

It is showing the size of the fiscal burden the market is being asked to absorb.

The higher the interest rate, the less the economy looks like capitalism and the more it looks like a machine searching for collateral.

The chart below makes that visible.

| Horizon | Public debt @ 5% | Public debt @ 7.5% | Public debt @ 10% | Gross debt @ 5% | Gross debt @ 7.5% | Gross debt @ 10% |

|---|---|---|---|---|---|---|

| 1 year | 1.9x | 3.1x | 4.3x | 2.4x | 3.9x | 5.4x |

| 5 years | 2.3x | 3.8x | 5.3x | 3.0x | 4.8x | 6.7x |

| 10 years | 2.9x | 4.8x | 6.8x | 3.9x | 6.3x | 8.8x |

The chart makes the pressure visible.

Under the public-debt model, a 5% effective interest-rate environment already requires a substantial expansion of the market-linked tax base. At 7.5%, the burden becomes extreme. At 10%, the market is no longer being asked merely to reflect economic growth. It is being asked to absorb fiscal strain.

Under the gross-debt version, the same pattern becomes even more severe. That does not mean gross debt is the correct market-refinancing base. It means the broader promise stack of the U.S. state is even larger than the fair market-facing model suggests.

Either way, the conclusion is the same:

The higher the interest rate, the more the system depends on asset inflation to keep the fiscal machine stable.

12. The reverse model: what happens if the stock market falls?

The Required Market Curve shows the upside pressure.

It asks how much the stock-market-linked taxable base must expand to keep the interest/revenue ratio stable.

But there is a second curve.

The panic curve.

What happens if the stock market falls?

This matters because if the market is part of the revenue system, then a market crash is not only a private-wealth event.

It becomes a fiscal event.

The model keeps the same basic assumptions:

starting federal revenue

debt held by the public

normal revenue growth

normal debt growth

effective interest rate

asset-sensitive tax base

But instead of asking how much the market must rise, we ask what happens if the market falls sharply over two quarters.

The shock scenarios are:

-10%, then -10%

-20%, then flat

-20%, then -20%

Because losses compound, the cumulative declines are:

| Market path | Cumulative decline |

|---|---|

| -10%, then -10% | -19% |

| -20%, then flat | -20% |

| -20%, then -20% | -36% |

The important point is that the tax effect is not necessarily linear.

If the stock market falls 20%, asset-linked tax receipts may not fall by exactly 20%.

They can fall by more.

Capital gains can disappear.

Stock options can go underwater.

RSUs vest at lower values.

Bonuses compress.

Founders delay selling.

Loss harvesting increases.

Business valuations fall.

High-end spending slows.

So the model uses two versions:

Linear case: asset-sensitive receipts fall in line with the market

Stress case: asset-sensitive receipts fall at 2x the market decline

Using an asset-sensitive tax base of $700 billion, the downside revenue shock looks like this:

| Market shock | Linear revenue loss | Stress revenue loss |

|---|---|---|

| -10%, then -10% | -$133B | -$266B |

| -20%, then flat | -$140B | -$280B |

| -20%, then -20% | -$252B | -$504B |

That is the first result.

A serious market fall can remove hundreds of billions of dollars from the most volatile part of the federal revenue system.

By itself, that does not collapse the state.

But it matters because it happens at exactly the wrong moment.

A market crash usually does not arrive alone.

It tends to arrive with weaker confidence, weaker growth expectations, tighter credit, lower capital gains, lower bonuses, and pressure on financial conditions.

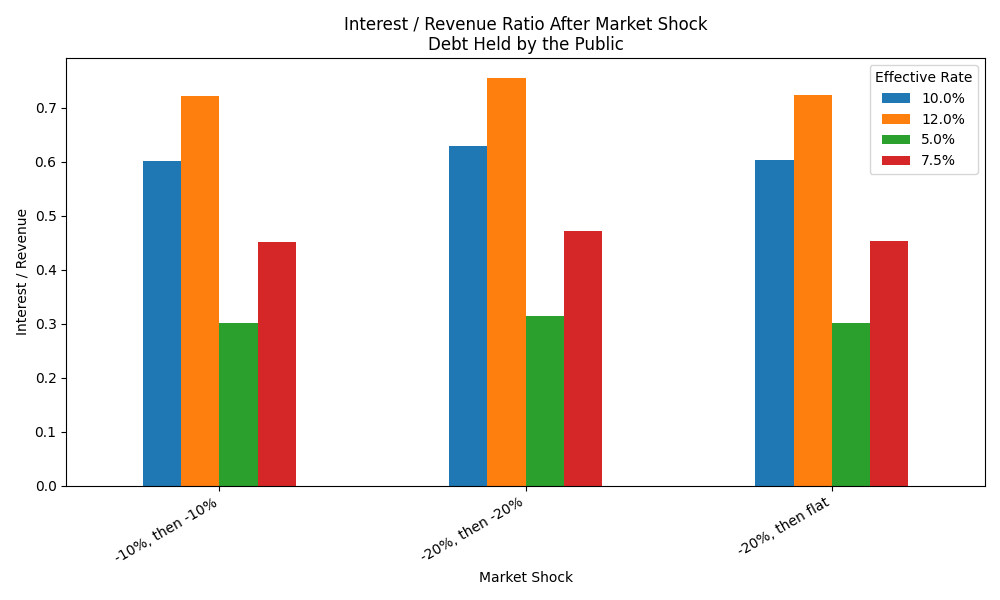

Now combine that revenue shock with higher effective interest rates.

Using debt held by the public as the main model, the interest/revenue ratio after the stress-case market shock becomes:

| Market shock | 5% rate | 7.5% rate | 10% rate | 12% rate |

|---|---|---|---|---|

| -10%, then -10% | 30% | 45% | 60% | 72% |

| -20%, then flat | 30% | 45% | 60% | 72% |

| -20%, then -20% | 31% | 47% | 63% | 75% |

This is the panic curve.

At 5%, the system is already above the warning zone.

At 7.5%, interest starts consuming nearly half of federal revenue.

At 10%, interest consumes more than 60% of revenue after the shock.

At 12%, the model is no longer describing normal fiscal politics.

It is describing emergency arithmetic.

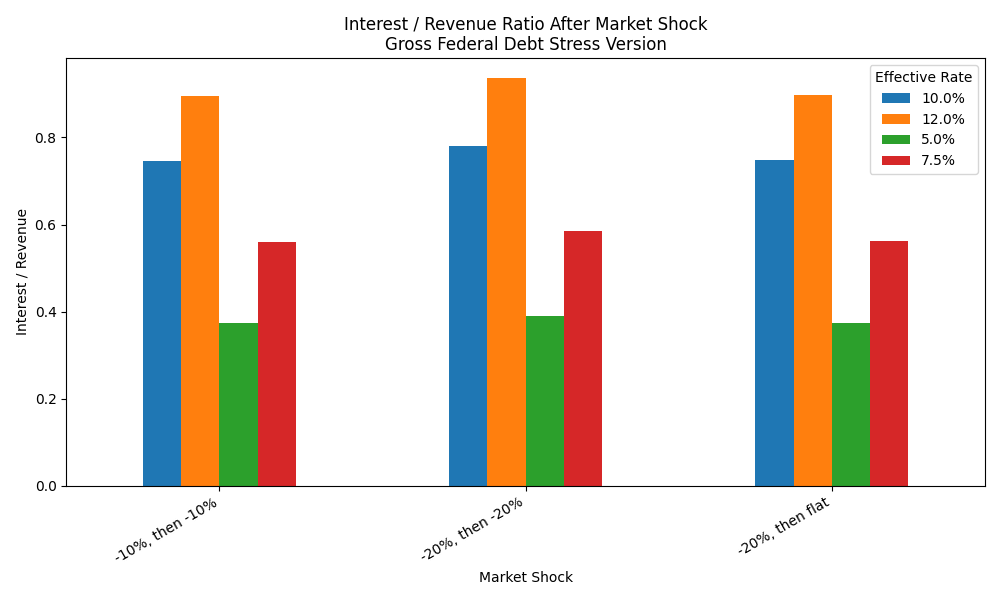

And if we run the same calculation against gross federal debt — the broader headline debt number approaching $40 trillion — the stress becomes even more severe:

| Market shock | 5% rate | 7.5% rate | 10% rate | 12% rate |

|---|---|---|---|---|

| -10%, then -10% | 37% | 56% | 75% | 90% |

| -20%, then flat | 37% | 56% | 75% | 90% |

| -20%, then -20% | 39% | 59% | 78% | 94% |

That does not mean gross debt is the cleanest refinancing base.

It is not.

Debt held by the public is the fairer market-facing model.

But the gross-debt version shows why the headline number still matters politically. It shows the size of the whole promise stack.

Either way, the conclusion is the same.

A falling stock market hits the system twice.

market falls

→ asset-linked tax receipts weaken

→ revenue falls

→ interest/revenue ratio worsens

→ deficit pressure rises

→ borrowing need rises

→ policy pressure increases

This is the reverse Asset-Tax Amplifier.

When the market rises, the amplifier helps the state.

When the market falls, the amplifier runs backward.

And when it runs backward while interest costs are rising, the system can deteriorate quickly.

That is why policymakers panic when markets fall hard.

Not because every investor must be protected.

Not because stocks are morally important.

But because a prolonged market decline damages the same revenue pipe the state needs to service the debt.

The upside model shows why the market has to grow.

The downside model shows why the market cannot be allowed to fall too far.

That is when a market event becomes a fiscal event.

Revenue Loss from a Market Shock

Interest / Revenue Ratio After Market Shock (Public Debt)

Interest / Revenue Ratio After Market Shock (Gross Federal Debt)

13. When does it become a problem?

The model does not say the system breaks because debt is high.

High debt is survivable if revenue grows fast enough.

It does not say the system breaks because stock valuations are high.

High valuations are survivable if earnings eventually arrive.

It does not say the system breaks because inflation stays above target.

Inflation is survivable if trust remains and the bond market keeps funding the state.

The problem begins when all three lines start moving against each other.

interest grows faster than revenue

asset-sensitive tax receipts cannot close the gap

market valuations exceed believable earnings growth

That is the danger point.

The U.S. can survive high debt.

It can survive high valuations.

It can survive inflation.

It cannot easily survive a situation where the debt needs the market to rise faster than earnings can justify, while inflation remains too high for easy rate cuts, while interest costs consume a rising share of federal revenue.

That is when the system leaves normal ranges.

This is the phase the AI stress-test is trying to identify.

Not collapse.

Constraint.

Collapse is dramatic. Constraint is quieter.

Constraint means the state still functions, but its choices narrow.

More revenue is pre-committed to interest.

More policy becomes market-sensitive.

More growth has to come from asset inflation.

More of the economy becomes dependent on a small number of companies carrying the index.

More political pressure builds around rates, liquidity, and stock prices.

The machine still runs.

But it has less room.

That is why the Required Market Curve matters.

At low effective interest rates, the market can behave like a market.

It can rise, fall, reprice, correct, and recover.

But as the effective interest rate rises, the market is asked to do more.

It is no longer merely reflecting expected profits.

It is helping support the fiscal machine.

At 5%, the requirement is uncomfortable.

At 7.5%, it becomes extreme.

At 10%, the market is being asked to absorb a burden that ordinary earnings growth may not be able to carry.

That is the critical transition.

The crisis is not high debt.

The crisis is not high stock prices.

The crisis is not inflation by itself.

The crisis is the moment the required market growth rate becomes larger than the believable earnings growth rate.

required market growth > believable earnings growth

That is when valuation stops being optimism and starts becoming system requirement.

This is the uncomfortable part.

If the market rises because earnings are rising, that is capitalism.

If the market rises because productivity is rising, that is growth.

If the market rises because innovation is creating real cash flows, that is value creation.

But if the market has to rise because the fiscal system needs the asset base to expand, then the market is no longer just pricing the future.

It is being recruited to finance the present.

That is where the Asset-Price State becomes visible.

It is not a formal policy.

It is not announced.

It is not written down as a programme.

But the incentives all point in the same direction.

The Treasury needs manageable funding conditions.

The Fed needs to avoid breaking the debt machine.

The White House needs the market high.

The tax system benefits when asset-linked income expands.

Mega-cap companies provide the scale.

AI provides the growth story.

Foreign capital provides the demand.

And the stock market becomes the place where all those pressures meet.

The danger point arrives when the story can no longer carry the numbers.

When earnings cannot justify the required multiple.

When AI capex cannot justify the valuation.

When inflation cannot be tolerated without damaging trust.

When rates cannot rise without damaging debt service.

When rates cannot fall without reigniting inflation.

When the market cannot fall without damaging revenue.

That is the box.

And once the system is inside that box, every policy choice becomes a trade-off between different forms of instability.

raise rates

→ protect inflation credibility

→ worsen debt service

→ pressure stocks

cut rates

→ protect debt service and stocks

→ risk inflation and dollar credibility

let stocks fall

→ restore valuation discipline

→ weaken tax receipts and confidence

support stocks

→ preserve the fiscal amplifier

→ deepen dependency on asset inflation

This is when the stock market stops looking like a normal market.

It becomes a load-bearing structure.

That does not mean stocks only go up.

It means large drawdowns become harder for the system to tolerate.

It means policy reacts faster.

It means liquidity support becomes easier to justify.

It means AI, mega-cap technology, defence, infrastructure, and national champions become more politically important.

It means the market becomes part of the state’s survival architecture.

That is the real problem.

Not that the market is high.

But that the market may now need to stay high.

And not merely stay high.

It may need to keep rising faster than the real economy can justify.

That is the constraint the model exposes.

| Condition | Normal version | Danger version |

|---|---|---|

| Debt | High, but serviceable | Interest grows faster than revenue |

| Stocks | Expensive, but earnings catch up | Required market growth exceeds believable earnings growth |

| Inflation | Above target, but trusted | Inflation needed for debt relief but damages credibility |

| Policy | Has room to tighten or loosen | Every move breaks another plate |

| AI narrative | Supports growth expectations | Becomes required to justify fiscal-scale valuations |

The problem begins when the market is no longer pricing growth, but being asked to manufacture fiscal capacity.

14. AI as the valuation excuse

This is where the AI narrative becomes structurally vital.

In a previous post, I argued that AI is increasingly being deployed as a technology of managed continuity.

Not collapse.

Not utopia.

Continuity.

AI appears everywhere because modern systems are under pressure everywhere: debt pressure, demographic pressure, wage pressure, energy pressure, institutional pressure, information pressure.

AI helps those systems measure more, optimise faster, compress costs, coordinate complexity, and preserve functionality.

That was the first layer.

This post adds the second layer.

AI is not only a continuity technology.

It is also a valuation technology.

The model shows why this matters.

If interest costs rise faster than normal revenue, the system needs asset prices to do more work. It needs the stock market to rise. It needs the asset-sensitive tax base to expand. It needs the largest companies to become larger. It needs the index to keep carrying wealth, confidence, capital gains, stock compensation, and federal receipts.

But markets cannot rise forever on fiscal need alone.

They need a story.

AI supplies that story.

productivity boom

automation

robotics

defence systems

data centres

energy demand

model infrastructure

software replacement

national competitiveness

This is why AI matters so much in the current market structure.

It is not just another technology cycle.

It is the only story large enough to justify the scale of market expansion the system now needs.

A normal software cycle is not enough.

A new phone cycle is not enough.

A better advertising model is not enough.

The market needs something larger.

It needs a story that can justify trillion-dollar companies becoming even larger.

It needs a story that can justify enormous data-centre spending.

It needs a story that can justify chip shortages, energy infrastructure, cloud expansion, defence integration, robotics, automation, and national-security investment.

It needs a story big enough to carry the index.

AI is that story.

This does not mean AI is fake.

That is the wrong argument.

AI may be real.

AI may be transformative.

AI may genuinely change software, labour, defence, education, logistics, medicine, manufacturing, administration, and energy demand.

But the fiscal system also needs AI to be real enough to justify the valuation regime.

That is the important distinction.

There is a difference between:

AI as technology

and:

AI as valuation permission

AI as technology asks:

What can these systems actually do?

AI as valuation permission asks:

What future cash flows can the market justify pricing today?

Those are not the same question.

And right now, the second question is doing enormous work.

AI allows the market to say:

yes, valuations are high

but productivity will rise

yes, capex is extreme

but infrastructure demand will explode

yes, labour is expensive

but automation will compress costs

yes, energy demand is rising

but that proves the scale of the boom

yes, mega-caps dominate the index

but they are the only companies large enough to build the future

This is why AI becomes more than a sector.

It becomes the narrative bridge between impossible numbers and believable markets.

Without AI, the Required Market Curve looks absurd.

With AI, the market gets a reason to suspend disbelief.

That does not mean the belief is wrong.

It means the belief is now load-bearing.

The AI story supports mega-cap valuations.

Mega-cap valuations support the S&P 500.

The S&P 500 supports household wealth, confidence, capital gains, stock compensation, and federal tax receipts.

Federal tax receipts support the debt-service machine.

That is the loop.

AI narrative

→ mega-cap valuation

→ index strength

→ asset-sensitive taxable income

→ federal revenue

→ debt-service support

This is where the two posts connect.

In the earlier post, AI appeared as managed continuity: a technology used by constrained systems to keep operating.

In this post, AI appears as valuation continuity: a story used by financial markets to keep pricing a future large enough to support the present.

Those are not separate arguments.

They are the same argument seen from different levels of the system.

Operationally, AI helps institutions manage constraint.

Financially, AI helps markets deny constraint.

That is why the timing matters.

AI arrives at the exact moment the old growth model is becoming harder to sustain.

Cheap debt is gone.

Demographic momentum is weaker.

Energy demand is rising.

Institutions are overloaded.

Interest costs are climbing.

The stock market needs a growth story big enough to carry extreme valuations.

And suddenly AI appears as the answer to almost every pressure point at once.

It promises productivity.

It promises labour compression.

It promises defence advantage.

It promises administrative efficiency.

It promises software replacement.

It promises energy demand large enough to justify new infrastructure.

It promises national competitiveness.

It promises growth without admitting that the old growth model is failing.

That is why AI is so useful to the system.

It is not only a tool.

It is an explanation.

It tells investors why valuations can stay high.

It tells companies why capex can explode.

It tells governments why industrial policy matters.

It tells voters that productivity is coming.

It tells markets that the future will be large enough to pay for the present.

That may be true.

But it has to become true.

That is the dangerous part.

AI now carries two burdens at once.

It has to become a real technology.

And it has to justify the market structure built on top of it.

If AI delivers slowly, the valuation story weakens.

If the valuation story weakens, the mega-caps weaken.

If the mega-caps weaken, the index weakens.

If the index weakens, the Asset-Tax Amplifier weakens.

And if the Asset-Tax Amplifier weakens while interest costs are rising, the fiscal machine loses one of its easiest support mechanisms.

That is why the AI trade is not just a technology trade.

It is a fiscal trade.

It is a dollar trade.

It is a state-capacity trade.

It is the market trying to believe in a future large enough to pay for the present.

AI may be the technology.

But it is also the story that allows the valuation regime to continue.

15. SpaceX and the national champion model

SpaceX is the perfect case study for this dynamic.

Not because it is fake.

That is not the argument.

SpaceX is obviously real. It launches rockets. It operates satellites. It has strategic value. It has military value. It has communications value. It has infrastructure value. It has national-prestige value.

That is exactly the point.

It is not being valued like a normal company because it is no longer being understood as a normal company.

It is being priced as a container for future strategic value.

launch capacity

satellite infrastructure

military communications

space logistics

national prestige

geopolitical leverage

future AI infrastructure

strategic optionality

In a normal valuation framework, the numbers are hard to justify.

At its IPO valuation, SpaceX was being priced at roughly ninety times trailing revenue. Not earnings. Revenue.

And the company had recently reported a multi-billion-dollar net loss.

In ordinary market conditions, that would look absurd.

A company trading at nearly one hundred times sales, with no conventional earnings support, would normally be treated as speculative excess.

But this is not an ordinary market condition.

That is the whole point of this post.

The market is not only pricing current cash flows.

It is pricing national necessity.

It is pricing strategic optionality.

It is pricing the possibility that SpaceX becomes one of the few private companies large enough to absorb trillions of dollars of valuation and still sound plausible.

That matters because the existing market is running out of believable containers.

Microsoft cannot grow tenfold from here under normal fundamentals.

Apple cannot grow tenfold from here under normal fundamentals.

Nvidia cannot carry the entire system forever.

The Magnificent Seven can support the index for a while, but if the Required Market Curve keeps rising, even they may not be enough.

So the market needs new containers.

It needs companies that can plausibly hold impossible valuations.

Not because the numbers already work.

But because the story is large enough.

That is why frontier assets matter.

AI

space

defence

energy infrastructure

robotics

satellite networks

sovereign cloud

data-centre empires

military communications

off-world compute

These are not normal sectors.

They are valuation frontiers.

They allow the market to say:

This is not just a company. This is infrastructure. This is national power. This is the future operating system of the state.

That changes the valuation logic.

A normal company is valued on earnings.

A growth company is valued on future earnings.

A national champion is valued on strategic necessity.

That is the new category.

SpaceX is not valued like a company.

It is valued like a piece of state infrastructure with private shareholders.

And once you understand that, the valuation starts to make sense in a different way.

Not as traditional finance.

As system finance.

The U.S. stock market needs assets large enough to carry global capital.

The fiscal system needs asset prices high enough to support the tax amplifier.

The political system needs symbols of national dominance.

The military system needs private infrastructure it can use without fully owning.

The AI system needs energy, compute, satellites, and frontier-scale ambition.

SpaceX sits at the intersection of all those needs.

That is why the market can price it at a level that looks irrational under ordinary accounting.

The accounting is not the product.

The strategic story is the product.

This is the national champion model.

A company becomes so entangled with state capacity, military logistics, communications, infrastructure, and future technology that the market stops asking only:

What did it earn last year?

And starts asking:

What part of the future state could this company own?

That is how impossible valuations become narratively possible.

This does not mean the valuation is safe.

It may be wildly dangerous.

It may be a bubble.

It may disappoint.

It may collapse if the story weakens.

But the function is clear.

The system needs frontier assets because ordinary assets are no longer large enough to absorb the required growth.

If the market has to double, triple, or quadruple under fiscal pressure, it cannot do that through ordinary companies selling ordinary products at ordinary margins.

It needs Star Trek assets.

It needs assets where the future is so large, so vague, so strategic, and so difficult to model that valuation discipline becomes suspended.

SpaceX gives the market that.

AI gives the market that.

Defence technology gives the market that.

Sovereign infrastructure gives the market that.

They are not just businesses.

They are valuation containers for a system that needs the asset base to keep expanding.

This is the deeper point.

When the required market growth rate exceeds believable earnings growth, the market does not immediately admit defeat.

It searches for a bigger story.

AI is one story.

SpaceX is another.

The national champion is the structure that joins them together.

That is why these companies matter so much.

They let the market price the future as if it is large enough to pay for the present.

At IPO pricing, the valuation was already close to 100x trailing revenue. If the stock trades materially above the IPO price, the sales multiple moves well beyond 100x. That is why the exact day-to-day market cap is less important than the valuation regime itself.

| Company type | Normal valuation anchor | New valuation anchor |

|---|---|---|

| Traditional company | Earnings, margins, cash flow | Business performance |

| Growth company | Future earnings | Market share and expansion |

| Mega-cap platform | Ecosystem control | Index weight and global capital absorption |

| AI infrastructure company | Future productivity | Compute, data, energy, automation |

| National champion | Strategic necessity | State capacity, defence, infrastructure, geopolitical leverage |

16. “Our currency, your problem”

John Connally famously told the world: