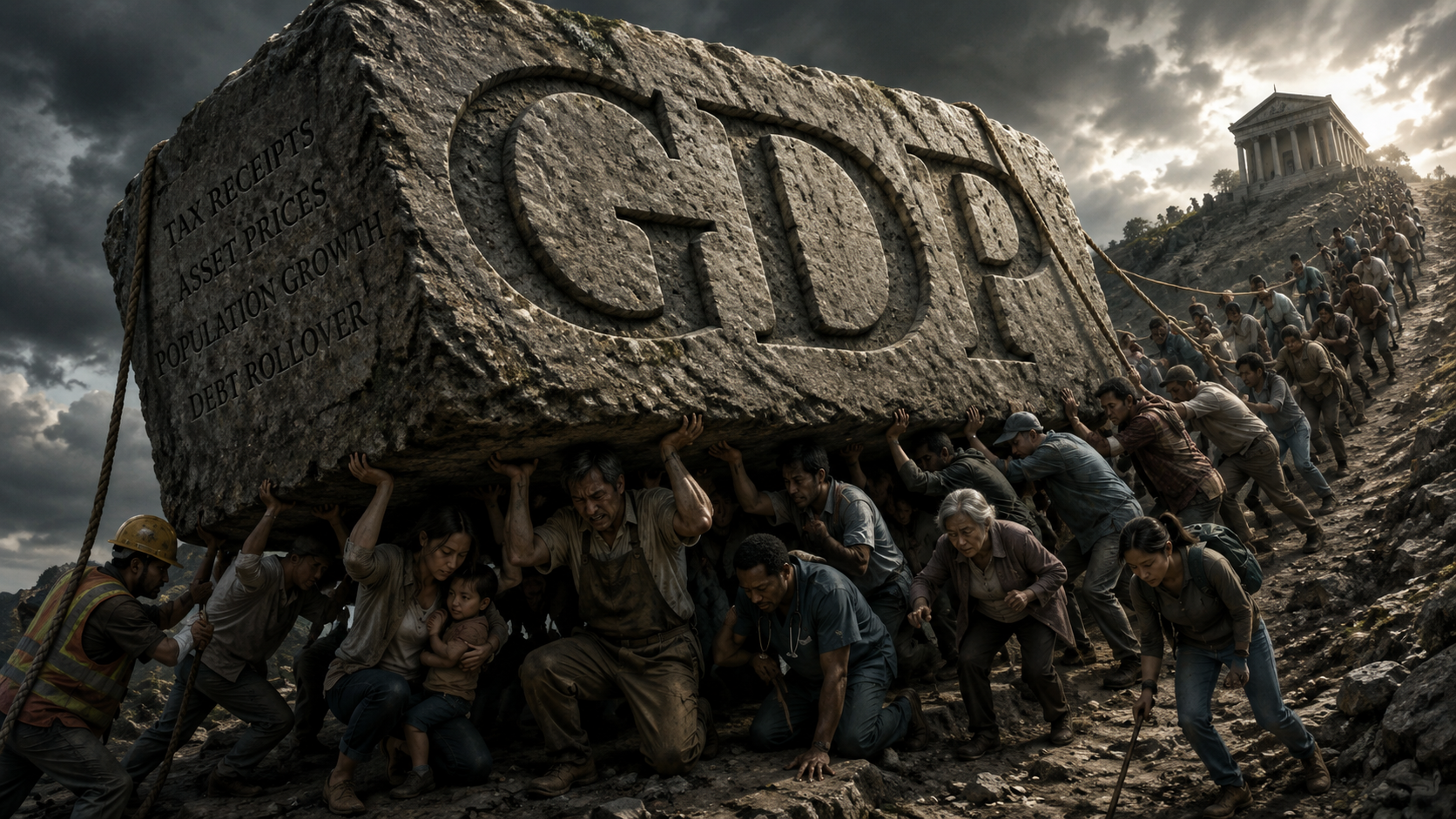

The State Optimized the Dashboard and Lost the Citizen

An AI-assisted model of how GDP optics, housing pressure, debt rollover, and fiscal constraint can hide citizen insolvency.

1. A Country Is Its Citizens

A country is not its GDP, its bond market, its housing index, or its stock-market capitalization. A country is its citizens.

That sounds obvious enough to be useless, but most modern economic dashboards quietly forget it. They measure the state, the asset market, the tax base, the debt stock, the growth rate, the investment flow, the headline employment number, the budget balance, the bond spread, and the index level. They do not directly measure whether citizens can stand on their own.

Can a worker afford a home? Can a renter build savings? Can a young family form without inherited wealth? Can a person leave a bad employer or landlord without immediate collapse? Can the next generation enter adult life without starting from debt, rent, dependence, and delay?

Those are not sentimental questions. They are solvency questions.

If a state preserves its balance sheet by weakening the citizen balance sheet, then the country has not been preserved. The loss has merely been moved downward.

That is the principle behind this post:

A state cannot be solvent if its citizens are becoming insolvent.

The usual macroeconomic dashboard can miss this entirely. GDP can rise while rent consumes the household. Tax receipts can rise while savings collapse. House prices can rise while ownership access disappears. The state can still borrow. The market can still approve. The press release can still say growth.

But underneath the dashboard, the citizen may be losing the capacity to build an independent life.

That is the gap this post tries to model.

Not collapse, not conspiracy, not one villain: a wrong objective function.

Modern states increasingly optimize for dashboard continuity: GDP, asset prices, tax receipts, population growth, capital inflows, debt rollover, and investor confidence. Those numbers matter. But the citizen needs something else: housing access, real wage power, savings resilience, public-service capacity, domestic productive depth, and the ability to say no.

This post calls that missing object citizen solvency.

The question is simple: can a country look successful while its citizens become less solvent?

If the answer is yes, then GDP is not enough. We need a way to measure what the dashboard is missing.

The rest of this post turns that question into a model: not a metaphor, not a mood, but a structure that can be inspected, tested, and broken.

2. The Dashboard State

Every system has an objective function, whether it admits it or not.

For a state, that objective function is usually implied rather than declared. It is scattered across budgets, forecasts, central-bank language, development plans, fiscal rules, housing schemes, investor presentations, migration targets, and growth projections.

But the revealed objective function is visible in what the system protects under pressure.

Modern states protect a familiar cluster of dashboard variables: GDP growth, tax receipts, asset values, debt rollover, institutional confidence, capital inflows, and the appearance of continuity.

None of these is automatically bad.

A state needs revenue. It needs functioning markets. It needs investment. It needs debt markets not to panic. It needs enough continuity for households, firms, banks, public services, and investors to plan around.

The problem is not that these dashboard metrics are fake.

The problem is that they are incomplete.

Goodhart’s law gives the warning: when a measure becomes a target, it stops being a good measure. A system can learn to move the number without improving the underlying condition the number was meant to represent.

That is the danger of the Dashboard State.

The point is not that the state is literally an AI. It is not.

The point is structural: a state optimizing GDP, tax receipts, asset prices, and debt rollover can suffer the same class of failure as any optimizer that overfits a proxy. The reward signal improves. The underlying target diverges.

In an AI system, that failure is called reward misspecification or specification gaming.

In a state, it appears as dashboard success with citizen insolvency underneath it.

That is the shared shape.

It can raise aggregate GDP through population growth while failing to expand housing, infrastructure, public services, and capital per worker at the same pace.

It can raise tax receipts through inflation and bracket creep while real disposable income falls.

It can protect bank balance sheets by protecting collateral values, while making housing less affordable for new entrants.

It can support renters or buyers with demand-side subsidies while doing too little to expand supply, allowing part of the support to flow into higher rents or higher prices.

It can preserve the appearance of wealth by keeping asset prices high while younger households lose the ability to buy those assets.

The dashboard improves.

The citizen balance sheet deteriorates.

That is not prosperity. It is a measurement failure.

The Dashboard State does not have to hate citizens, intend harm, or require conspiracy. It only has to reward policies that improve headline continuity while failing to measure whether those same policies weaken household independence.

That is how the wrong objective function becomes dangerous.

This isn’t because GDP is useless, markets are bad, or confidence doesn’t matter. It is simply because a system eventually becomes what it measures, protects, and rewards.

If the dashboard measures GDP, tax receipts, asset values, population growth, debt rollover, and investor confidence, then policy will tend to protect those things.

If it does not also measure housing access, real wage power, savings resilience, ownership access, public-service capacity, family formation, and exit power, then those things can deteriorate while the official dashboard still says success.

This is why the model in this post does not begin with GDP.

It begins with the citizen.

The next step is to turn that divergence into a simple architecture: dashboard variables on one side, citizen-solvency variables on the other.

3. Citizen Solvency

Citizen solvency is the ability of a typical working-age household to participate in the economy without structural dependence.

It is not income.

A high wage does not create solvency if rent absorbs it. A growing economy does not create solvency if a household cannot reach ownership inside it. A rising stock market does not create solvency if the median household owns almost none of it.

Income is a flow.

Solvency is a position.

The number that matters is not only what a household earns, but what it has left after the essential costs of living. That remaining space — the discretionary surplus — is what becomes savings, what absorbs shocks, what enables a move, and what lets a person refuse a bad employer or a bad landlord without immediate collapse.

Citizen solvency therefore has several dimensions:

housing access

rent burden

ownership access

real wage power

savings resilience

debt-service burden

family-formation feasibility

public-service access

exit power

This is a starting point, not a finished list.

Some of these dimensions overlap. Housing access, rent burden, and ownership access are all different readings of the same underlying pressure: the cost and attainability of shelter. The model has to account for that relationship rather than triple-count it.

But the list has one advantage over GDP: every item asks whether the household can actually live inside the economy the state says is succeeding.

In the model, these dimensions become a Citizen Solvency Dashboard.

That dashboard is not a single magic number. Housing stress, wage power, savings resilience, debt burden, public-service access, and exit power are not the same quantity. Collapsing them too early would create false precision.

They should first be shown separately.

Then the model can ask whether they are moving together or diverging.

Together, they answer one question:

Is policy increasing household independence, or increasing dependency pressure?

The model does not begin with loaded historical analogies. It begins with measurable dependence: rent that cannot be escaped, debt that cannot be cleared, and the absence of any savings buffer that would let a household say no.

That is functional dependence.

And it is what the dashboard exists to detect before it hardens.

Each of these dimensions can be measured from public data. In the next section, they stop being a list and become the variables of a model you can run.

4. The Model in One Page

This post is not asking you to accept a metaphor.

It is proposing a test.

The test is simple: can the national dashboard and the citizen balance sheet move in opposite directions?

Put the two side by side.

The dashboard measures the continuity of the state:

GDP · tax receipts · asset prices · population growth

capital inflows · debt rollover · headline employment · bond-market confidence

The citizen solvency readout measures what the dashboard does not see directly:

housing access · rent burden · ownership access · real wage power

savings resilience · family-formation feasibility · public-service access · exit power

The model’s job is to watch for divergence between them.

| When this rises | And this happens | The model calls it |

|---|---|---|

| Dashboard | Citizen solvency rises | Real growth |

| Dashboard | Citizen solvency falls | Dashboard growth |

| Debt | Future capacity rises | Productive transfer |

| Debt | Future entry costs rise | Regressive transfer |

| Population | Capacity scales with it | Scalable growth |

| Population | Capacity does not scale | Population-capacity illusion |

| Asset prices | Ownership access rises | Broad wealth formation |

| Asset prices | Ownership access falls | Entrant exclusion |

That table is the model in plain English.

Everything else is the machinery that makes each row measurable.

Underneath both readouts sits the part policy actually acts on: the structural economy. This is the real system of rates, debt, wages, rents, house prices, housing supply, public-service capacity, productivity, tax revenue, and external constraints.

The dashboard and the citizen-solvency readout are measurements of what that system produces. They are not causes in their own right.

That distinction matters.

You cannot fix a country by editing its dashboard. You change the structural economy, then read the consequences off the citizen.

A fourth layer extends the same logic across time. The future citizen layer asks whether today’s policy improves or worsens the position of the next person trying to enter adult economic life.

Did today’s debt buy future capacity?

Or did it preserve current continuity while handing the next generation higher entry costs?

That question gets its own section later, because it is the intergenerational heart of the model. For now, the point is simpler: debt is not judged by whether it exists. It is judged by what it buys.

flowchart TD

P[Policy / Debt / Regulation] --> S[Structural Economy<br/>rates · wages · rents · housing supply · productivity · public services]

S --> D[State Dashboard<br/>GDP · tax receipts · asset prices · debt rollover]

S --> C[Citizen Solvency Readout<br/>housing access · savings · ownership · exit power]

S --> F[Future Citizen Layer<br/>future capacity · future entry costs · future tax burden]

D -. compared with .-> C

C -. projected into .-> F

The model deliberately avoids collapsing these readouts into one magic number. Housing stress, wage power, savings resilience, public-service access, and exit power are different quantities. A single score would create false precision.

The first version should show the dimensions separately.

Then the model can ask where they move together, where they diverge, and which policy choices produce the divergence.

This matters because citizen solvency is also a chosen readout. It is better than GDP for the question this post asks, but it is not a magic escape from Goodhart’s law.

Any metric can become dangerous if it becomes the only target.

So the durable contribution is not merely replacing GDP with citizen solvency. It is building a system of readouts that can contradict each other: dashboard, citizen, future citizen, fiscal, external, and capacity.

The contradiction detector is the safety mechanism.

The AI layer appears later. For now, the important point is that the claim can be decomposed into variables, readouts, and falsification tests.

AI is useful here only insofar as it helps turn a vague complaint into an inspectable system: explicit variables, structural causes, measurement readouts, and data patterns that would weaken or break the thesis.

For example:

If dashboard gains consistently coincide with improving citizen solvency,

the thesis weakens.

If debt-funded capacity consistently lowers future entry costs,

the debt critique weakens.

If population growth is matched by housing, infrastructure, public services,

and capital deepening, then the population-capacity illusion is not present.

That is the contribution.

It offers inspection, not certainty.

The main post gives the readable model. The appendix gives the runnable one: the dynamic causal model, the variable ledger, the normalization choices, the scenario definitions, the sensitivity tests, and the code that regenerates the charts.

The claim and the machine that tests it should ship together.

5. The Population-Capacity Gap

The problem described here is not population, and it is not the people who arrive.

The problem is a gap.

A state can increase the number of people living, working, renting, consuming, paying tax, and transacting inside an economy. That will often make the aggregate dashboard look stronger. More people can mean more total consumption, more total rent payments, more total employment, more total tax receipts, and a larger headline GDP number.

But aggregate GDP is not what a household lives on.

A household lives inside the per-capita and per-household reality: income per person, housing per household, capital per worker, infrastructure per user, public-service capacity per citizen, and disposable surplus after essential costs.

That is the distinction the dashboard can miss.

Total output can rise while output per person stalls.

Total housing can rise while housing per household falls.

Total tax receipts can rise while service access per citizen deteriorates.

Total employment can rise while capital per worker weakens.

This reframes the issue away from people versus citizens, and toward demand versus capacity.

Population growth is one source of demand. So is household formation. So is income growth. So is credit expansion. So is investor demand for housing and land. The model does not ask whether more people arrived. It asks whether the capacity to absorb demand scaled with the demand.

The model therefore has to measure growth against capacity:

housing supply per household

public-service capacity per citizen

transport, water, and energy capacity per user

capital per worker

productivity per worker

construction throughput

If those measures rise with demand, population growth can be real growth. It can increase labour supply, tax receipts, entrepreneurship, cultural depth, productive energy, and national capacity.

But if demand rises faster than capacity, the dashboard can improve while the citizen balance sheet weakens.

When demand outruns capacity, the consequences are not mysterious. Rents rise because housing supply lags household formation. Public services strain because demand expands faster than delivery. Savings weaken because shelter and essentials absorb more disposable income. Ownership recedes because entry prices move faster than real wages.

The state reads the aggregate and calls it growth.

The citizen lives inside the gap and experiences it as pressure.

In the model, this becomes a capacity-gap test.

The old version of the formula would be too loose if it simply subtracted housing, infrastructure, public services, and capital from population growth as if they all had the same unit. They do not.

The safer version is to treat the capacity gap as a bottleneck problem, not a simple subtraction between unlike quantities.

Let \(G_t\) represent the capacity gap at time \(t\):

$$ G_t = D_t - C_t $$Where \(D_t\) is demand pressure and \(C_t\) is the system’s absorptive capacity.

Demand pressure is a weighted combination of domestic strains:

$$ D_t = w_1 \Delta P_t + w_2 \Delta F_t + w_3 \Delta H_t + w_4 \Delta S_t + w_5 \Delta Q_t $$Where:

\(ΔP_t\) = population growth

\(ΔF_t\) = household formation

\(ΔH_t\) = housing demand

\(ΔS_t\) = public-service demand

\(ΔQ_t\) = credit / income demand pressure

Capacity is constrained by the tightest bottleneck:

$$ C_t = \min \left( \Delta H^{comp}_t, \Delta I_t, \Delta S^{cap}_t, \Delta K^{worker}_t, \Delta B_t \right) $$Where:

\(ΔH^{comp}_t\) = housing completions per household

\(ΔI_t\) = infrastructure capacity per user

\(ΔS^{cap}_t\) = public-service capacity per citizen

\(ΔK^{worker}_t\) = capital deepening per worker

\(ΔB_t\) = construction / administrative throughput

Capital Deepening versus Capital Dilution

This is also where the productivity story lives.

If labour supply rises while the physical, administrative, technological, and housing capital available per worker fails to rise with it, the economy can grow in aggregate while weakening the productive base beneath each worker.

That is the distinction between capital deepening and capital dilution.

Capital deepening means workers are matched by more tools, infrastructure, housing, systems, energy capacity, administrative throughput, and productive investment.

Capital dilution means more workers are added to a system whose supporting capacity has not scaled.

In simplified terms:

$$ \text{Capital Deepening}_t = \Delta \left(\frac{K}{L}\right)_t > 0 $$$$ \text{Capital Dilution}_t = \Delta \left(\frac{K}{L}\right)_t < 0 $$Where \(K\) represents the capital stock broadly understood — housing, infrastructure, tools, productive systems, public capacity, and administrative throughput — and \(L\) represents labour.

This is not a claim about the workers.

It is a claim about the investment environment into which workers are added.

flowchart TD

P[Population growth] --> D[Demand pressure D_t]

F[Household formation] --> D

H[Housing demand] --> D

Q[Credit / income demand shock] --> D

HC[Housing completions] --> C[Absorptive capacity C_t]

I[Infrastructure capacity] --> C

S[Public-service capacity] --> C

K[Capital per worker] --> C

B[Construction / administrative throughput] --> C

C --> G{Capacity gap G_t > 0?}

D --> G

G -->|Yes| X[Rent pressure · service strain · capital dilution · savings erosion]

X --> Y[Citizen solvency falls]

G -->|No| Z[Demand absorbed by capacity]

Z --> W[Citizen solvency stable or improves]

This distinction matters because it prevents the model from blaming people for arriving.

The harm is not population itself.

The harm is population growth, or any demand growth, being used as a substitute for the housing, infrastructure, capital deepening, construction capacity, and productivity that would allow it to become lived solvency.

That is the population-capacity illusion: the dashboard celebrates aggregate volume while the citizen pays for the missing capacity.

The later Canada and Ireland sections apply this test directly.

The visual test is simple:

population growth / household formation

versus

housing completions / capacity expansion

The point is not the population line by itself.

The point is the gap.

6. The Future Citizen Balance Sheet

The present citizen balance sheet is only half the picture.

The other half is intergenerational.

Public debt is often described as borrowing from the future, as if that settled the matter. It does not. Borrowing from the future is not automatically wrong.

There is an old and orthodox case for borrowing: long-lived public capital can be funded across the generations that benefit from it. If a future citizen helps pay for a school, a grid, a rail line, a water system, a hospital, or a stock of public housing they actually use, the debt is not simply a burden. It is part of the cost of inherited capacity.

A future citizen may rationally inherit a liability if they also inherit the capacity that liability created.

Debt used to build homes, energy systems, transport, schools, water infrastructure, health capacity, productive industry, and real wage capacity can improve the future citizen balance sheet.

The future citizen inherits a bill.

But they also inherit useful capital.

That can be legitimate.

The problem is different when borrowing, guarantees, subsidies, or future tax commitments are used in ways that preserve present claims without building future capacity.

If policy stabilizes incumbent asset values, defends collateral, preserves income streams from scarce assets, or socializes downside risk, the intent does not have to be malicious for the incidence to change.

The present holder receives protection.

The future entrant receives part of the bill.

Worse, the future entrant may also face a higher cost of entry into the same asset system that policy helped preserve.

This is the concept this section turns on:

asymmetric incidence across time.

One operation has two sides.

The gain lands with current holders.

The cost lands with future entrants.

It is tempting to call this double-entry bookkeeping across generations, but the image is only useful if we notice where it breaks. In normal double-entry accounting, the entries balance inside one ledger. Here, the credit is posted to one cohort and the debit to another.

That is the asymmetry.

The future citizen balance sheet therefore has to show both sides: what the future inherits as capacity, and what the future inherits as burden.

| Policy route | Present effect | What the future citizen inherits |

|---|---|---|

| Debt used to build housing, transport, energy, schools, water, or health capacity | More capacity now | Public capital, lower future pressure, improved entry conditions |

| Debt used to raise productivity and domestic productive capacity | Slower payoff, but deeper productive base | Higher wage capacity and stronger resilience |

| Debt or guarantees used to defend incumbent asset values and collateral | Stabilized current balance sheets | Debt service plus higher future entry price |

| Support for demand without matching supply | Current relief or preserved income streams | Higher rent or price baseline if capacity does not expand |

| Deferral of infrastructure and service investment | Lower present political/fiscal pressure | Public-capital backlog and weaker future service access |

The same fiscal action can look similar on the state dashboard and produce opposite entries on the future citizen’s books.

That is why the question is not simply:

Can the state service the debt?

The question is:

What did the debt buy for the citizens who will service it?

If the answer is housing, infrastructure, energy capacity, public services, productivity, or lower future costs, the transfer may be productive.

If the answer is merely asset continuity, collateral protection, rent preservation, or another year of dashboard stability, the transfer may be regressive across generations.

The worst version occurs when future citizens are assigned the liabilities of a system that also makes their entry into adult life more expensive.

They do not merely inherit debt.

They inherit debt service plus higher house prices.

Debt service plus higher rents.

Debt service plus weaker public services.

Debt service plus reduced ownership access.

Debt service plus lower discretionary surplus.

That is why the model treats the future citizen position as a ledger, not a slogan:

Future Citizen Position — ledger, not scalar:

inherits as capacity:

public capital

housing stock

productive capacity

wage capacity

ownership access

lower future non-discretionary costs

inherits as burden:

debt service

tax burden

rent baseline

asset-entry cost

public-service backlog

reduced public-investment room

lower discretionary surplus

This is not a literal accounting identity. The terms have different units, different timings, and different data sources. The ledger is a structured comparison, not a single number pretending to settle the argument.

There is also a discount-rate problem. Any attempt to collapse future costs and future benefits into a present value depends on how heavily the model discounts the future. A low discount rate makes future harms loom larger. A high market-style discount rate can make them appear smaller.

The model should not hide that choice.

It should expose it.

The technical appendix can make the discount rate adjustable and show how the conclusion changes when it moves.

None of this is invented from nothing. Economists already have tools for parts of the problem: generational accounting, fiscal incidence analysis, public-capital analysis, and the old distinction between borrowing for investment and borrowing for current consumption.

The contribution here is to connect those tools to citizen solvency.

The model does not ask only whether the state balance sheet survives.

It asks whether the next generation can own, save, form households, absorb shocks, access services, and build independent lives inside the economy they inherit.

That is the future citizen test.

Debt is legitimate when it buys future citizen capacity.

Debt becomes dangerous when it preserves present claims while raising the future citizen’s cost of entry.

The next section turns this ledger into a policy classifier.

7. What Did the Debt Buy?

Section 6 gave the principle: a fiscal action helps or harms the next generation depending on whether they inherit capacity or only the bill.

This section turns that principle into a test that can be run on a single policy.

A policy should not be judged only by its stated purpose.

It should be judged by where its benefits and burdens land.

That is the incidence rule, and it is what keeps the classifier honest. Almost every policy is described as protecting the economy, stabilizing the system, helping households, or supporting growth. The model does not begin with the press release. It begins with the ledger.

So every debt-funded or future-funded policy gets one question:

Did it raise future capacity at least as much as it raised future burden?

Operationally, that means:

Did the policy reduce future non-discretionary costs,

raise productive capacity,

improve ownership access,

or strengthen future wage power

enough to justify the debt service it leaves behind?

If yes, the debt may be investment.

If no, it is a transfer.

The model then classifies what kind.

| Debt is used to… | Where the burden and benefit land | Class | What would confirm it |

|---|---|---|---|

| Build housing, transport, energy, schools, water systems | Future citizens inherit the asset and a lower cost of entry | Productive | Housing completions and public capital rise; future entry costs ease |

| Fund skills, health capacity, domestic industry, productivity | Future citizens inherit stronger wage capacity and resilience | Productive | Productivity, real wages, and capacity per worker improve |

| Smooth a genuine temporary shock | Burden and capacity roughly balance | Neutral / stabilizing | Productive capacity is preserved; no lasting entry-cost rise |

| Support demand without expanding supply | Current relief, but higher future price or rent baseline | Regressive | Supports rise, supply stays flat, prices or rents rise |

| Support buyer demand without expanding housing supply | Present buyers receive help; future entrants face higher prices | Regressive | House-price-to-income worsens; ownership access falls |

| Defend asset values or collateral without reform | Current values are stabilized; entry cost is passed forward | Regressive | Asset values hold while younger ownership falls |

| Load liability and raise the cost of entry into the same assets | Future citizens pay twice: debt service plus higher entry cost | Extractive | Debt-service burden rises and entry costs rise together |

The labels can be debated.

They should be.

The important part is that the classifier does not stop at intention. It asks what the policy actually changed.

A productive transfer gives the future citizen something useful enough to justify the burden: housing, public capital, productive capacity, lower future living costs, stronger wage power, or better access to ownership.

A neutral or stabilizing transfer buys time during a genuine shock. It may not transform the future citizen balance sheet, but it prevents productive capacity from being destroyed.

A regressive transfer passes burden forward without enough matching capacity. It may help someone today, and it may even be necessary in a crisis, but if it does not expand supply or reduce future costs, it can leave the future citizen worse off.

An extractive transfer is the severe case: the future citizen inherits both the liability and a higher price of entry into the system the liability helped preserve.

This distinction matters because a state can always say it is acting responsibly.

A rent support may prevent immediate hardship.

A bank rescue may prevent wider damage.

A temporary subsidy may buy time.

But buying time is not the same as buying capacity.

The classifier therefore asks what happened after the intervention.

Did the state use the time to build homes, infrastructure, productive capacity, and lower future costs?

Or did it preserve the existing price structure and pass the liability forward?

That is where the Future Citizen Balance Sheet becomes operational.

It does not ask whether the policy sounded responsible.

It asks what future citizens received in exchange for the burden.

In the runnable version, the classifier does not produce a single truth score. It produces a structured comparison: a Citizen Solvency Dashboard, a capacity-gap reading, a future-citizen ledger, and a policy classification with the evidence behind it.

Representative inputs include:

GDP per capita

debt-service-to-revenue

house-price-to-income

rent-to-income

housing completions versus population growth

ownership by age cohort

median wage growth

public capital proxies

household savings

The full input and output spec belongs in the appendix and repository.

For now, the point is simple:

Policy claim:

this protects the economy

Model question:

what did it buy for the future citizen?

The classifier is only as good as the data it receives.

The next sections feed it real data: Canada, where the divergence is visible at scale, and Ireland, where the same test matters because the margin for error is smaller.

8. Canada: The Capacity Gap at Scale

Canada is the first place to run the model.

Canada is included not because it failed uniquely, but because it makes the population-capacity gap visible at scale.

For years, the Canadian dashboard could still look successful. Aggregate GDP grew. Population grew. Tax receipts rose. Asset values remained high. Major cities continued to look globally attractive. On the surface, the country looked like a large, stable, expanding advanced economy.

But the citizen balance sheet was telling a different story.

The useful question is not whether the economy became larger in total.

The useful question is whether the typical household became more solvent inside that larger economy.

That is where Canada matters.

Run the model from Section 5.

Population growth is demand growth. It can be good. It can support scale, enterprise formation, tax receipts, urban depth, labour supply, and long-term national capacity.

But only if capacity scales with it.

Housing must scale.

Infrastructure must scale.

Public services must scale.

Capital per worker must scale.

Productivity must scale.

Real wages must preserve access to shelter, savings, ownership, and family formation.

When those things move together, the classifier returns scalable growth.

When population rises but capacity lags, the capacity-gap flag fires.

Canada is useful because the relevant indicators can be tested directly.

The first test is the dashboard illusion.

Evidence requirement:

Compare aggregate GDP with GDP per capita over the high-population-growth period.

Likely sources:

Statistics Canada, OECD.

Model question:

Did the country grow in total while output per person stalled or fell?

If aggregate GDP rises while GDP per capita stagnates or declines, the dashboard and the citizen are no longer reading the same economy. The state can report expansion. The household can experience deterioration.

That is not a contradiction.

It is the model working.

The second test is the physical bottleneck.

Evidence requirement:

Compare population growth / household formation with housing completions.

Likely sources:

Statistics Canada, CMHC.

Model question:

Did the country add households faster than it added homes?

This is the core Canada chart.

The visual point is not immigration.

The visual point is the gap.

If demand rises faster than housing completions, the missing homes do not disappear from the system. They reappear as rent pressure, bidding pressure, longer commutes, crowding, delayed ownership, and reduced household surplus.

The third test is citizen solvency.

Evidence requirement:

Compare rent-to-income, house-price-to-income, real wages, savings resilience, and ownership access by age cohort.

Likely sources:

Statistics Canada, CMHC, OECD, Bank of Canada.

Model question:

Did asset values rise while entry access weakened?

This is where dashboard growth becomes citizen pressure.

A rising housing market can look like national wealth from one side of the ledger. It can support collateral values, bank balance sheets, household net worth for existing owners, and political confidence.

But for new entrants, the same price increase is not wealth.

It is a higher entrance fee.

That is why the model separates asset prices from ownership access. If asset prices rise while ownership access falls, the model does not call that broad wealth formation. It calls it entrant exclusion.

Canada also needs the productivity test.

Evidence requirement:

Track productivity, business investment, and capital per worker.

Likely sources:

Statistics Canada, OECD, Bank of Canada.

Model question:

Did the economy add workers faster than it added the capital, tools, infrastructure, and productivity required to raise output per worker?

This matters because population growth without capital deepening can preserve aggregate activity while weakening the per-worker foundation of prosperity.

That is the deeper failure mode.

The country becomes larger.

But the citizen’s claim on capacity becomes smaller.

As Section 5 argued, population is not the failure variable.

The gap is.

The model is making a narrower claim:

Population growth is a stress test on state capacity.

Canada chose, or allowed, rapid demand growth. The failure was that complementary capacity did not arrive at the same speed: homes, infrastructure, public services, productive capital, and wage capacity.

The state counted population as an asset.

But the citizen experienced unbuilt capacity as a liability.

That is the Canada lesson.

The failure was not too many people; it was too little capacity, and too much confidence that aggregate growth would automatically translate into household solvency.

In a runnable version of the model, Canada would not receive a slogan. It would receive a diagnostic readout.

Runnable model inputs:

population growth

household formation

housing completions

GDP growth

GDP per capita growth

rent burden

house-price-to-income

ownership by age cohort

productivity growth

capital per worker

real wage growth

household savings resilience

Runnable model outputs:

capacity-gap reading

citizen-solvency pressure map

dashboard/citizen divergence flags

policy classification

evidence-backed charts

The result would not be a single truth score.

It would be a map of where the dashboard and the citizen diverged.

When the gap widens, the pressure usually appears first in rent.

Then in savings.

Then in ownership access.

Then in family formation.

Then in political trust.

By the time the dashboard admits failure, households have often been living inside the failure for years.

Canada is not included here to make the essay about Canada.

Canada is included because it makes the model concrete.

It shows how a state can grow in aggregate while the entrance price to adult life rises faster than the citizen’s capacity to pay it.

The next question is whether the same model travels.

Ireland is the harder test: a smaller economy, a more distorted GDP dashboard, less monetary room, and a housing constraint with less margin for error.

First Canada Run: Demand Versus Capacity

The Canada section should not remain only a description of what the model would look for. The table below gives the first empirical readout.

It maps the public-data indicators used in this section onto the model’s capacity-gap logic: dashboard growth, demand pressure, housing-capacity response, and the resulting flag.

The table does not claim to be the final Canada model. It is the first v0.1 application: enough to show whether the Canada case is merely rhetorical, or whether the population-capacity mechanism appears in the data.

| Model test | Public-data readout | Calculation / comparison | Model output |

|---|---|---|---|

| Demand pressure | Household formation, 2024 | 482,000 net new households | demand_pressure_input = high |

| Capacity response | Net housing completions, 2024 | 276,000 net units | capacity_response_input = constrained |

| Capacity gap | Formation minus completions | 206,000-unit gap; 1.75x demand-to-completion ratio | canada_capacity_gap_flag = fired |

| Required build-rate gap | Required vs projected annual completions to 2035 | 290,000 required vs 227,000 projected; 63,000/year shortfall (1.28x) | canada_required_build_rate_gap_flag = fired |

| Citizen divergence | Wage, rent, ownership, resilience series | Not yet populated in the first run | dashboard_citizen_divergence = provisional |

Source: Parliamentary Budget Officer, Household Formation and the Housing Stock (2025). The capacity-gap flag fires because household formation ran at 1.75 times net completions, a 206,000-unit gap in a single year, and the required build rate to close it by 2035 sits 28% above the projected baseline. The dashboard/citizen divergence row stays provisional on purpose: confirming it requires the wage, rent, and ownership-by-cohort series, which the first run does not yet carry.

9. Ireland: The Small-State Stress Test

Ireland is not Canada.

That distinction matters.

Canada showed the population-capacity gap at scale: a large country, with its own currency and central bank, adding demand faster than it added housing, infrastructure, capital deepening, and productivity.

Ireland is a different test.

It is smaller. More open. More exposed. It sits inside the euro. It does not control its own currency. It cannot devalue its way out of a competitiveness shock. It cannot set monetary policy around Irish domestic conditions alone.

That gives Ireland less room for error.

But Ireland’s deeper problem is not only constraint.

It is measurement.

Headline GDP is unusually sensitive to multinational activity. That does not mean Ireland is fake. It does not mean the activity is imaginary. It means GDP is too volatile and too globally mediated to serve, by itself, as the readout for Irish citizen solvency.

In model terms, GDP is a valid input for some questions and a miscalibrated input for others. It can overstate domestic strength in one period and exaggerate apparent weakness in another.

If the question is:

How large is the activity booked through the Irish economy?

GDP matters.

But if the question is:

Can a typical Irish household build an independent life inside the Irish economy?

GDP is not enough.

The model therefore needs a measurement-correction layer.

For Ireland, the dashboard cannot be read directly. It has to be triangulated through domestic-capacity measures such as GNI*, modified domestic demand, domestic income, housing access, rent burden, ownership access, public-service capacity, and domestic productive depth.

That is why Ireland belongs in the model.

Ireland belongs in the model not because it is uniquely doomed, but because it is unusually revealing.

It shows what happens when the national dashboard looks strong before the citizen balance sheet has been properly measured.

The Irish dashboard can report extraordinary output, strong tax receipts, rising asset wealth, and high employment.

The model asks what those readouts mean after correction:

Which output is domestic capacity?

How concentrated are the receipts?

Who can enter the asset base?

Do wages buy independence after rent, tax, childcare, transport, and housing costs?

Those questions are not political slogans. They are feature-selection problems.

Irish GDP is not the citizen-solvency readout. It is one signal, to be compared with domestic measures that better approximate the lived economy.

Measurement correction:

headline GDP

compared with

GNI*

modified domestic demand

domestic income

real wage capacity

housing access

public-service capacity

If headline GDP rises while domestic citizen capacity does not deepen, the model raises a dashboard-divergence flag.

That is the first Irish test.

The second test is fiscal concentration.

Ireland’s corporation-tax receipts can make the state dashboard look safer than it really is. High receipts improve the fiscal picture. They can reduce borrowing pressure, fund public spending, support transfers, and create the appearance of national strength.

But if a large share of those receipts comes from a small number of multinational firms, the model cannot treat the revenue base as ordinary domestic capacity.

It has to flag concentration risk.

The danger is not that corporation tax is bad.

The danger is that recurring domestic obligations may be funded from concentrated, volatile, externally exposed receipts.

That creates a future-citizen risk.

If windfall receipts are converted into durable capacity — housing, infrastructure, energy systems, water systems, schools, healthcare capacity, transport, domestic productive capital — then the future citizen inherits assets.

If windfall receipts are consumed into permanent commitments without matching capacity, then the future citizen inherits the obligation without the asset.

That brings Ireland back to the question from Section 7:

What did the money buy?

Capacity?

Or continuity?

The third Irish test is citizen solvency.

A country can look rich while ordinary households face rising rents, delayed ownership, weak domestic capacity, and dependence on a narrow tax base.

This is not the same as saying Ireland is poor.

The claim is sharper:

Ireland can look rich while producing weaker future citizen solvency.

That is much harder to dismiss, because it does not deny the dashboard. It audits it.

The Irish question is:

Is Ireland becoming richer in a way that makes Irish citizens more independent, or richer in a way that makes them more dependent?

That is the whole test.

If GDP rises but GNI* and domestic capacity lag, the output is a measurement-distortion flag.

If corporation-tax receipts rise while concentration risk rises with them, the output is a fiscal-fragility flag.

If housing wealth rises while younger households are excluded from ownership, the output is an entrant-exclusion flag.

If population and employment rise while housing, infrastructure, and public services lag, the output is a capacity-gap flag.

If public spending rises but durable capacity does not, the policy is classified as continuity spending rather than productive transfer.

In a runnable version, Ireland becomes a different model instance from Canada.

Runnable model inputs:

headline GDP

GNI*

modified domestic demand

domestic income

corporation-tax concentration

windfall corporation-tax share

recurring spending dependence

housing completions

rent burden

house-price-to-income

ownership access by age cohort

domestic productivity

domestic capital formation

population growth

public-service capacity proxies

eurozone constraint flag

Runnable model outputs:

GDP distortion flag

fiscal-concentration risk flag

domestic-capacity reading

housing-access pressure map

citizen-solvency divergence flag

future-citizen liability risk

external-constraint sensitivity

The output is not a verdict — Ireland good, Ireland bad, Ireland doomed.

The output is a diagnostic map.

It shows where the dashboard is reliable, where it needs correction, and where apparent national strength may not translate into citizen solvency.

That is why the section needs at least three evidence hooks.

Figure requirement:

headline GDP versus GNI* / modified domestic demand

Visual point:

the headline dashboard is not the same as domestic citizen capacity.

Figure or table requirement:

corporation-tax concentration / windfall corporation-tax share

Visual point:

fiscal strength can hide concentration risk.

Figure requirement:

house-price-to-income, rent burden, or ownership access by age cohort

Visual point:

asset wealth and citizen access can move in opposite directions.

The mistake would be to claim that Ireland is poor, or conversely, that Irish GDP is entirely fake. Neither is true.

That is not the claim either.

The claim is that Ireland’s dashboard needs correction before it can be trusted as a measure of citizen solvency. If multinational activity surges, GDP can make the economy look stronger than the domestic citizen readout. If multinational activity reverses, GDP can make the economy look weaker than the domestic citizen readout. The problem is not the direction of the distortion. The problem is treating the distorted measure as the citizen readout.

And the model must remain falsifiable.

If Ireland converts concentrated fiscal windfalls into durable public capital, builds enough housing, deepens domestic productive capacity, improves infrastructure, and lowers the entrance cost to adult life, then the citizen-solvency readout should improve.

The readout should show that.

It is not a doom machine.

It is an audit layer.

Ireland therefore exposes the next part of the model: the external constraint. A state can want to improve citizen solvency and still face limits set by currency regimes, global capital, multinational tax structures, energy dependence, import exposure, bond markets, and European institutions.

That is where the model has to go next.

First Ireland Run: Dashboard Versus Domestic Readout

The Ireland section also needs a first empirical readout.

Ireland is not used here as another Canada. It tests a different part of the model: whether headline GDP can diverge from domestic-capacity measures, and whether fiscal strength can hide concentration risk.

The table below maps the public-data indicators onto the Ireland model instance. GDP/GNI* divergence does not prove citizen poverty. It proves measurement distortion. Citizen pressure has to be read separately through household-side indicators such as income, deprivation, rent burden, ownership access, or savings resilience.

| Model test | Public-data readout | Calculation / comparison | Model output |

|---|---|---|---|

| GDP vs domestic demand | GDP growth vs Modified Domestic Demand, Q1 2026 | -12.1% vs +0.6%; 12.7pp gap | ireland_gdp_mdd_divergence_flag = fired |

| GDP vs GNP | GDP growth vs GNP growth, Q1 2026 | -12.1% vs +1.5%; 13.6pp gap | ireland_gdp_gnp_divergence_flag = fired |

| Multinational vs domestic | MNE-dominated vs domestic sectors, Q1 2026 | -27.1% vs +0.4%; 27.5pp gap | ireland_multinational_domestic_sector_divergence_flag = fired |

| Fiscal concentration | Top three groups’ share of corporation tax, 2024 | 46% (about €13bn) | ireland_fiscal_concentration_flag = fired |

| Citizen pressure | Household-side indicators (SILC, rent, income) | Not inferred from GDP | ireland_dashboard_citizen_divergence_flag = not assessed |

Sources: CSO, Quarterly National Accounts Q1 2026 (Provisional); IFAC corporation-tax concentration analysis (2024). Note the direction: in this quarter headline GDP fell 12.1% while domestic demand rose, so GDP is understating domestic conditions, not exaggerating them. That is the “distortion in either direction” point made concrete. A single quarter this extreme is itself the argument: GDP swings like this precisely because multinational accounting moves it, which is why it cannot serve as the citizen readout. The load-bearing evidence here is not the one quarter but the structural figure beneath it: the 46% corporation-tax concentration and the persistent gap between GDP and domestic measures. The citizen-pressure row is deliberately not assessed: GDP/GNI* and sector divergence prove measurement distortion and fiscal-concentration risk, not household poverty, which has to be read separately from SILC, rent, and income data.

10. The External Constraint

The model now leaves the closed domestic system.

No small open economy operates in isolation. A state can control parts of its housing policy, tax policy, planning system, public investment, infrastructure delivery, and domestic regulation. But it does not set every condition under which those choices are made.

It does not set the global cost of capital, the dollar system, the European monetary regime, global energy prices, China’s industrial cost structure, or global tax rules by itself.

A serious model has to include those constraints without exaggerating them.

The state still has agency.

But agency operates inside boundary conditions.

That is the external-constraint layer.

In the model, external constraints are not excuses. They are exogenous inputs: variables the state does not fully control, but which shape its domestic policy room.

external constraint

-> domestic policy room

-> capacity delivery

-> citizen solvency

That middle layer matters.

External forces do not automatically determine citizen outcomes. They change the price, feasibility, timing, and risk of domestic choices. The state still decides whether to build housing, reform planning, invest in public capital, deepen productivity, diversify its tax base, and protect the future citizen balance sheet.

But it makes those decisions inside a system.

The United States matters because it shapes the global financial environment. The dollar system, Treasury market, equity-market depth, dollar liquidity, and safe-asset demand influence the benchmark conditions under which other states borrow, invest, and compete for capital.

That is the rate channel.

When global rates rise, smaller states do not set the benchmark. They absorb it through sovereign borrowing costs, mortgage rates, investment hurdles, asset valuations, and fiscal pressure.

There is also an allocation channel.

The United States can absorb global capital at a scale few countries can match. Its financial markets offer depth, liquidity, collateral, and perceived safety. When global savings are pulled toward US assets, other states compete against that benchmark for investment.

That does not require a conspiracy.

It is a structural feature of the system.

The US can run a financial model that smaller states cannot easily copy, because the world still treats US financial assets as core collateral. That gives the US more room to roll debt, sustain asset valuations, absorb global capital, and tolerate fiscal stress for longer.

Countries outside that centre face a different constraint: they compete for capital, absorb global rates, and are compared against deeper, more liquid markets.

That is the financial gravity well.

China matters differently.

It is not primarily a financial gravity well in this model. It is an industrial pressure input: manufacturing scale, export capacity, state coordination, cost structure, and tradable-sector pressure.

For Ireland, this channel should not be overstated. Ireland is not Germany. But any small Western economy trying to rebuild domestic production does so in a world where China can manufacture at scale and often at prices domestic firms struggle to match.

That does not make reindustrialisation impossible.

It makes it harder.

The eurozone matters more directly for Ireland.

Ireland does not control its own currency. It does not set monetary policy for Irish domestic conditions alone. The ECB rate becomes an external input into Irish mortgages, credit conditions, sovereign financing, business investment, and housing affordability.

That does not mean Ireland has no choices.

It means Ireland has fewer release valves.

A country with its own currency can, in some circumstances, absorb pressure through exchange-rate movement, domestic monetary policy, or inflation. Ireland’s adjustment channels are narrower. Pressure is more likely to move through wages, prices, fiscal policy, housing, public services, emigration, and dependence on European institutions.

EU fiscal rules matter for the same reason.

If the model recommends public investment to build capacity, it must also ask whether the state has legal, fiscal, and market room to borrow and spend. A capacity-building plan is not only an economic idea. It is a policy-room problem.

Energy and import dependence also matter.

A small open economy is often a price-taker for energy, construction inputs, food, machinery, technology, and intermediate goods. When external prices rise, the effect is not abstract. It enters the citizen balance sheet through heating, electricity, transport, rent, food, construction costs, and mortgage affordability.

Global tax rules matter too.

Ireland’s corporation-tax position is not set entirely in Ireland. International tax agreements, US policy, EU rules, profit-shifting changes, and global minimum-tax frameworks can change the value of the tax base Ireland has come to depend on.

That is why multinational dependency appears in the external-constraint layer as well as the Ireland section.

It affects GDP measurement.

It affects tax receipts.

It affects fiscal risk.

It affects the future citizen balance sheet if recurring domestic obligations are funded from concentrated, externally exposed receipts.

The model therefore treats the external world as a constraint vector.

US financial gravity:

affects benchmark rates, dollar liquidity, capital flows,

asset valuations, and fiscal stress

Eurozone monetary regime:

affects Irish interest rates, mortgage costs,

credit conditions, and adjustment channels

EU fiscal rules:

affect public-investment room and capacity-building options

Energy and import exposure:

affects household costs, construction costs,

inflation, and domestic productive capacity

China industrial pressure:

affects tradable sectors, import prices,

and domestic production options

Multinational dependency:

affects Irish tax revenue, GDP measurement,

and fiscal fragility

Global tax rules:

affect the durability of corporation-tax receipts

and the stability of the fiscal dashboard

This keeps the argument measured.

The housing crisis is still primarily a domestic capacity failure.

Planning, supply, land, credit, public housing, infrastructure, construction throughput, and policy design matter enormously.

Global forces do not replace that story.

They amplify it.

External rates can worsen mortgage affordability. Import prices can raise construction costs. Capital flows can affect asset valuations. EU fiscal rules can shape the investment envelope. But homes are still permitted, financed, serviced, connected, and built through domestic systems.

That is the agency layer.

A state cannot set every external variable.

But it can decide whether to convert available resources into capacity.

It can decide whether windfall receipts become durable assets.

It can decide whether planning systems increase throughput or preserve scarcity.

It can decide whether public capital lowers future entry costs.

It can decide whether debt buys capacity or continuity.

So the point is not that Ireland has no choices.

The point is that choices made inside a dependency structure are still choices, but their cost, timing, and feasibility are constrained.

flowchart TD

A[US financial conditions] --> B[Global rates and capital flows]

C[China industrial pressure] --> D[Tradable-sector and import-price pressure]

E[Eurozone monetary regime] --> F[Limited monetary adjustment]

G[Multinational dependency] --> H[Tax and GDP exposure]

I[Energy and import exposure] --> J[Imported cost pressure]

K[EU fiscal rules] --> L[Public-investment headroom]

B --> M[Domestic policy room]

D --> M

F --> M

H --> M

J --> M

L --> M

M --> N[Capacity delivery]

N --> O[Housing, infrastructure, public services, productivity]

O --> P[Citizen Solvency Readout]

P --> Q[Exit pressure / emigration / trust loss]

Q --> M

The earlier diagrams show how policy affects the economy and how the economy is read by the dashboard and the citizen. But a society is not a one-way machine. Citizen solvency feeds back into politics.

When households lose independence, the pressure does not remain private. It becomes voting behaviour, protest, distrust, emigration, institutional stress, and eventually a demand to change the objective function itself.

This is what makes the state an adaptive optimizer rather than a static machine.

If the dashboard is rewarded for long enough, the groups that benefit from dashboard preservation gain incentives to defend it. Asset holders defend asset prices. Institutions defend continuity. Fiscal systems defend the revenue base. Political actors defend the numbers that make them look competent.

The proxy does not merely measure the system.

It begins to organize power around itself.

flowchart TD

P["🏛️ Policy / Debt / Regulation"]

S["⚙️ Structural Economy<br/>rates · wages · rents · housing · productivity · services"]

D["📊 State Dashboard<br/>GDP · tax receipts · asset prices · debt rollover"]

C["🧍 Citizen Solvency<br/>housing access · savings · exit power · family formation"]

F["👶 Future Citizen Balance Sheet<br/>future capacity · future entry costs · future tax burden"]

T["🗳️ Political Feedback<br/>voting · protest · trust · emigration · legitimacy"]

O["🎯 Objective Function Update<br/>dashboard preservation ↔ citizen solvency"]

P --> S

S --> D

S --> C

S --> F

D -. "official success signal" .-> O

C -. "lived reality signal" .-> T

F -. "intergenerational pressure" .-> T

T --> O

O --> P

C -->|"dependency pressure rises"| T

T -->|"policy demand changes"| P

classDef policy fill:#e8f0ff,stroke:#2f5fd0,stroke-width:2px,color:#111;

classDef structure fill:#fff4df,stroke:#d99000,stroke-width:2px,color:#111;

classDef dashboard fill:#e8ffe8,stroke:#2d9b45,stroke-width:2px,color:#111;

classDef citizen fill:#ffe8e8,stroke:#d04a4a,stroke-width:2px,color:#111;

classDef future fill:#f2e8ff,stroke:#7a4fd0,stroke-width:2px,color:#111;

classDef politics fill:#fff0fa,stroke:#c13f91,stroke-width:2px,color:#111;

classDef objective fill:#f7f7f7,stroke:#555,stroke-width:3px,color:#111;

class P policy;

class S structure;

class D dashboard;

class C citizen;

class F future;

class T politics;

class O objective;

In a runnable version, this layer does not produce a moral verdict. It produces a sensitivity map.

External constraint inputs:

US benchmark rates

dollar liquidity conditions

ECB policy rate

eurozone fiscal constraints

sovereign spread / borrowing cost

energy and import exposure

construction-input cost pressure

multinational tax exposure

global tax-rule sensitivity

tradable-sector pressure

External constraint outputs:

policy-room score

fiscal-sensitivity flag

imported-cost pressure

capital-flow pressure

tax-base exposure flag

external-dependency map

citizen-solvency shock sensitivity

That is what keeps the model honest.

It does not let the state blame everything on the outside world.

It also does not pretend the outside world is irrelevant.

It asks a narrower, more useful question:

Given the external constraint,

what domestic capacity can still be built,

and what happens to the citizen balance sheet if it is not?

At this point, the model has become multidimensional.

It includes dashboard metrics, citizen solvency, housing capacity, debt classification, the future citizen balance sheet, country-specific measurement correction, fiscal concentration, and external constraints.

Ordinary political argument cannot police all of those moving parts reliably.

That is where the AI audit layer enters.

11. The AI Audit Layer

At this point, the post could become a normal macro essay.

That would not be enough.

The model now has too many moving parts for prose alone to audit reliably: dashboard metrics, citizen-solvency variables, housing capacity, debt classification, future-citizen burdens, country-specific measurement corrections, fiscal concentration, external constraints, feedback loops, and time lags.

A normal essay can gesture at those relationships.

A model has to expose them.

That is where the AI layer enters.

The AI layer is not an oracle, a prophecy, or a mechanism to prove the author right. Its narrower job is to make the argument inspectable.

It helps turn prose into structure.

It helps turn structure into tests.

It helps turn vague claims into things a reader can challenge.

In this model, AI is used for seven tasks:

Some of this is AI.

Some of it is ordinary software.

The AI is useful for the linguistic and adversarial work: extracting hidden claims from prose, identifying ambiguous terms, proposing variables, finding contradictions, generating counterarguments, and checking whether the model has smuggled a conclusion into its own definitions.

The software is useful for the mechanical work: storing variables, running scenarios, comparing series, calculating subindices, checking thresholds, and producing repeatable reports.

The point is not to pretend that AI discovers truth.

The point is to stop language from hiding claims.

Macroeconomic arguments often hide inside words.

Words like:

growth

prosperity

competitiveness

sustainability

affordability

resilience

reform

investment

prudence

capacity

can mean almost anything unless they are forced into structure.

The model asks:

What variable does this word refer to?

What data source would measure it?

What direction should it move?

What lag should we expect?

What would prove the claim wrong?

Take affordability.

In prose, affordability can mean a feeling, a political complaint, a mortgage rule, a rent burden, a deposit barrier, or a house-price-to-income ratio.

The model has to split it apart:

affordability:

rent_to_income

house_price_to_income

deposit_years_required

mortgage_payment_to_income

ownership_access_by_age_cohort

residual_income_after_non_discretionary_costs

Once that happens, two people arguing about “affordability” may discover they were not arguing about the same thing.

One was talking about rent.

One was talking about deposits.

One was talking about mortgage payments.

One was talking about ownership access for younger households.

That is one AI contribution: not final judgement, but decomposition.

There is a second contribution, which is easier to miss.

AI can act as a lens-finder.

It can surface the frame that a domain specialist may not reach because the specialist is already inside the domain’s native vocabulary. In this post, the useful frame is not only fiscal. It is also an objective-function problem.

The state has a dashboard.

The dashboard becomes a proxy.

The proxy becomes the target.

The target diverges from the human layer.

That is why the economics, the systems language, and the AI-alignment language meet here.

The AI did not prove the frame.

It helped locate it.

The model, the data, the falsification tests, and the reader still have to decide whether the frame earns its keep.

The first methodological correction is that this is not a static DAG.

A true DAG is acyclic. But an economy contains feedback loops.

Rent affects savings.

Savings affect ownership access.

Ownership access affects household formation.

Household formation affects housing demand.

Housing demand affects rent.

If those are drawn inside one static graph, the model becomes circular.

The cleaner representation is a time-indexed causal graph.

Within a single time slice, the graph can remain acyclic.

Across time steps, feedback appears.

Rent_t

→ Savings_t

→ OwnershipAccess_t+1

→ HouseholdFormation_t+1

→ HousingDemand_t+2

→ Rent_t+2

The same is true for asset prices and credit:

AssetPrices_t

→ Collateral_t

→ CreditAvailability_t+1

→ HousingDemand_t+1

→ AssetPrices_t+2

And for fiscal pressure:

InterestCost_t

→ FiscalRoom_t+1

→ PublicInvestment_t+1

→ Capacity_t+2

→ RevenueBase_t+3

→ InterestStress_t+3

Ireland adds another loop:

RentBurden_t

→ SavingsPressure_t

→ ExitPressure_t+1

→ Emigration_t+1

→ LabourSupply_t+2

→ TaxBase_t+2

→ PublicServiceCapacity_t+3

This matters because it stops the model from pretending the economy is simpler than it is.

It also forces us to specify lags.

Housing supply does not respond instantly.

Debt interest does not reset instantly.

Productivity does not appear instantly.

Tax receipts do not always respond instantly.

Migration responds to conditions, but also changes conditions.

The model needs time.

The second methodological correction is that the structural layer and the measurement layer must be separate.

The model cannot draw an arrow from rent to the Citizen Solvency Dashboard and pretend that is causal if rent is one of the dashboard’s components.

That is measurement, not causation.

So the model has two layers.

Structural layer:

rates

debt

wages

rent

house prices

housing supply

population-capacity gap

productivity

tax revenue

public services

external constraints

Measurement / readout layer:

Citizen Solvency Dashboard

Future Citizen Balance Sheet

The structural layer describes the economy.

The measurement layer reads the state of the citizen.

Keeping those layers separate prevents circularity and makes the model inspectable. Edges, lags, weights, data sources, normalization choices, thresholds, and scenarios become explicit surfaces for review rather than hidden assumptions inside prose.

That is the standard the model has to meet.

A model that cannot be attacked cannot be trusted.

The AI audit layer therefore sits beside the model, not inside it.

It is a sidecar.

It checks the claims, the variables, the edges, the lags, the sources, the normalization, and the falsification tests.

It does not become the economy.

It audits the representation.

ai_audit_layer:

role: audit_not_oracle

tasks:

- decompose_claims_into_variables

- separate_structural_nodes_from_readouts

- map_claims_to_data_requirements

- generate_scenario_matrix

- run_sensitivity_checks

- generate_falsification_tests

- generate_adversarial_counterclaims

constraints:

- no_oracle_claims

- no_unsourced_outputs

- expose_assumptions

- preserve_uncertainty

- separate_model_outputs_from_policy_values

- flag_missing_data

- flag_circularity

- flag_false_precision

The AI layer also creates risks: hallucination, source laundering, false precision, overfitting, and political judgement disguised as technical scoring.

That is why every output must be bound to one of four things:

a source

an assumption

a test

a declared uncertainty

An edge requires a mechanism.

A weight requires evidence.

A conclusion requires a falsification test.

If none can be supplied, the claim is marked as speculative.

That is the discipline.

The AI does not remove judgement; it makes it explicit.

With the audit layer defined, the next step is to define the model itself: the inputs, subindices, transformations, classifications, outputs, and evidence hooks that make up the Citizen Solvency Model.

12. The Citizen Solvency Model

The Citizen Solvency Model is built to test two divergences.

The first is immediate:

Can the national dashboard improve while current citizen solvency deteriorates?

The second is intergenerational:

Can current state continuity be maintained by weakening the future citizen balance sheet?

Those are the two core diagnostics.

The first catches dashboard growth.

The second catches asymmetric transfer across time.

A state can look stable now by passing higher entry costs, weaker public capacity, and larger liabilities to the next person trying to enter adult economic life.

That is why the model has to read both the present citizen and the future citizen.

The dashboard variables are familiar:

GDP

tax receipts

asset prices

debt rollover

population growth

capital inflows

headline employment

bond-market confidence

debt / GDP

interest / revenue

These are the numbers modern states already watch closely. They matter. A state cannot ignore growth, tax receipts, debt service, investment, employment, or financial stability.

But they are not the citizen balance sheet.

There is also a bridge variable:

GDP per capita

GDP per capita is useful because it decomposes aggregate growth. If total GDP rises but GDP per person stalls or falls, the model has found an early dashboard/citizen divergence. But GDP per capita is still not citizen solvency. It does not tell us whether the median household can pay rent, build savings, access ownership, or absorb shocks.

The citizen variables are different.

They include shelter, income power, resilience, services, and exit capacity.

shelter / access:

rent burden

house-price-to-income

time-to-deposit

ownership access

housing availability

income / resilience:

real wage power

residual discretionary income

savings resilience

household debt-service exposure

non-discretionary cost stack

family / services:

family-formation feasibility

childcare cost burden

public-service capacity

healthcare / education access

exit / autonomy:

exit power

ability to leave a bad landlord

ability to leave a bad employer

ability to move without insolvency

External dependency is not a citizen variable. It belongs in the external constraint layer: eurozone rules, global rates, multinational tax exposure, energy/import dependence, and global capital conditions.

The model asks whether the dashboard variables and citizen variables move together or apart.

If GDP rises and citizen solvency rises, the model classifies that as real growth.

If GDP rises while rent burden, entry costs, service strain, debt exposure, and household fragility rise with it, the model classifies that as dashboard growth.

The purpose of the model is not to prove doom, but to distinguish between policy paths.

Model Architecture

The model has architecture layers and readouts.

Those are not the same thing.

The architecture is:

Structural layer:

rates

debt

wages

rents

house prices

housing supply

productivity

tax revenue

public services

infrastructure

administrative throughput

External constraint layer:

global rates

eurozone regime

EU fiscal rules

capital flows

energy/import exposure

multinational tax exposure

global tax rules

tradable-sector pressure

Measurement / readout layer:

Citizen Solvency Dashboard

Future Citizen Balance Sheet

Policy classifier:

productive / stabilizing / regressive / extractive

AI audit sidecar:

checks assumptions

checks data sources

checks lags

checks weights

checks normalization

checks scenarios

generates falsification tests

The readouts are:

Current Citizen Solvency Dashboard

Future Citizen Balance Sheet

capacity-gap flags

dashboard/citizen divergence flags

policy classification

dependency pressure

The architecture describes how the model is built.

The readouts describe what the model emits.

Schema Preview

The full model belongs in a technical appendix or repo.

But the main post needs enough schema to make the claim inspectable.

citizen_solvency_model:

version: "csm.v0.1"

diagnostics:

dashboard_vs_current_citizen:

question: "Can the national dashboard improve while current citizen solvency deteriorates?"

outputs:

- real_growth

- dashboard_growth

- citizen_solvency_divergence

current_continuity_vs_future_citizen:

question: "Can current continuity be maintained by weakening the future citizen balance sheet?"

outputs:

- productive_transfer

- stabilizing_transfer

- regressive_transfer

- extractive_transfer

inputs:

dashboard:

growth:

- gdp_growth

- gdp_per_capita_growth

- headline_employment

fiscal:

- tax_receipts

- debt_to_gdp

- interest_to_revenue

- debt_rollover

financial:

- asset_prices

- capital_inflows

- credit_growth

- bond_market_confidence

citizen:

shelter_access:

- rent_burden

- house_price_to_income

- time_to_deposit

- ownership_access

- housing_availability

income_resilience:

- real_wage_power

- residual_discretionary_income

- savings_resilience

- household_debt_service_exposure

- non_discretionary_cost_stack

public_capacity:

- public_service_capacity

- childcare_cost_burden

- healthcare_access

- education_access

autonomy:

- exit_power

future_citizen:

- future_debt_service

- future_tax_burden

- future_housing_entry_cost

- future_rent_burden

- public_capital_stock

- productive_capacity

- wage_capacity

- future_ownership_access

external_constraints:

- global_rates

- eurozone_constraint

- eu_fiscal_rules

- energy_import_exposure

- multinational_tax_exposure

- global_tax_rule_sensitivity

architecture: